Household Debt Rose Modestly; Delinquency Rates Remain Elevated

Press Release

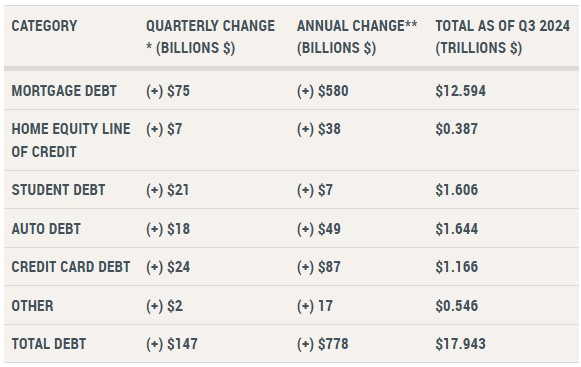

New York, NY – November 13, 2024 – The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit. The report shows total household debt increased by $147 billion (0.8%) in Q3 2024, to $17.94 trillion. The report is based on data from the New York Fed’s nationally representative Consumer Credit Panel. It includes a one-page summary of key takeaways and their supporting data points.

The New York Fed also issued an accompanying Liberty Street Economics blog post examining the evolution in aggregate debt to income ratios and what that suggests about Americans’ ability to manage their debt obligations.

“Although household balances continue to rise in nominal terms, growth in income has outpaced debt,” said Donghoon Lee, Economic Research Advisor at the New York Fed. “Still, elevated delinquency rates reveal stress for many households, even amid some moderation in delinquency trends this quarter.”

Mortgage balances increased by $75 billion from the previous quarter and reached $12.59 trillion at the end of September. HELOC balances increased by $7 billion, representing the tenth consecutive quarterly increase since Q1 2022, and stood at $387 billion. Credit card balances increased by $24 billion to $1.17 trillion. Auto loan balances saw a $18 billion increase and stood at $1.64 trillion. Other balances, which include retail cards and other consumer loans, were effectively flat, with a $2 billion increase. Student loan balances grew by $21 billion, and now stand at $1.61 trillion.

The pace of mortgage originations increased slightly from the pace observed in the previous four quarters, with $448 billion of newly originated mortgages in Q3. Aggregate limits on credit card accounts increased modestly by $63 billion, representing a 1.3% increase from the previous quarter. Limits on HELOC increased by $9 billion, the tenth consecutive quarterly increase.

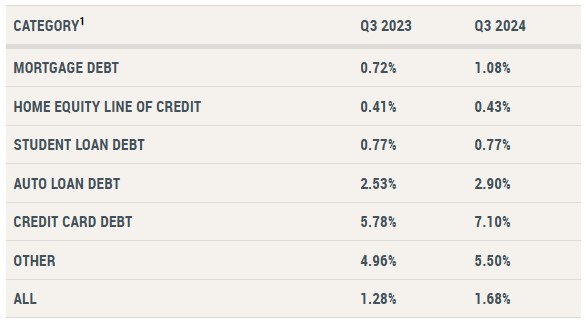

Aggregate delinquency rates edged up from the previous quarter, with 3.5% of outstanding debt in some stage of delinquency. Delinquency transition rates were mixed. Credit card delinquency rates improved, with 8.8% of balances transitioning to delinquency compared to 9.1% in the previous quarter. Early delinquency transitions for auto loans and mortgages worsened slightly, rising by 0.2 and 0.3 percentage points respectively. About 126,000 consumers had a bankruptcy notation added to their credit reports this quarter, a small decline from the previous quarter.

Household Debt and Credit Developments as of Q3 2024

Flow into Serious Delinquency (90 days or more delinquent)

About the Report

The Federal Reserve Bank of New York’s Household Debt and Credit Report provides unique data and insight into the credit conditions and activity of U.S. consumers. Based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample drawn from anonymized Equifax credit data, the report provides a quarterly snapshot of household trends in borrowing and indebtedness, including data about mortgages, student loans, credit cards, auto loans, and delinquencies. The report aims to help community groups, small businesses, state and local governments, and the public to better understand, monitor, and respond to trends in borrowing and indebtedness at the household level. Sections of the report are presented as interactive graphs on the New York Fed’s Household Debt and Credit Report webpage and the full report is available for download.

1 Rates represent annualized shares of balances transitioning into delinquency. Flow into serious delinquency is computed as the balances that have newly become at least 90 days late in the reference quarter divided by the balances that were current of less than 90 days past due in the previous quarter.

Contact

Connor Munsch

(347) 224-1175

Connor.Munsch@ny.frb.org

Source: NYFRB

Related:

Fed Reserve Sees Auto Loan and Credit Card Delinquency Worsening in Q1 2024

New York Fed – Auto Loan Delinquencies Continue to Rise – New York Fed – Auto Loan Delinquencies Continue to Rise – New York Fed – Auto Loan Delinquencies Continue to Rise New York Fed – Auto Loan Delinquencies Continue to Rise – Auto Loan Delinquencies Continue to Rise

Auto Loan Delinquencies Continue to Rise – Delinquency – Credit Union Collections – Credit Union Collectors – Lending – Auto Loan

Household Debt Rose Modestly; Delinquency Rates Remain Elevated

More Stories

Auto Loan Fraud Losses Have Tripled, But the Number of Fraud Cases Is Falling

Federal Banking Agencies Issue New Guidance on Immigration-Related Credit Risk

The Auto Finance Paradox

Early Bird Registration for CCUCC 2026 Ends August 14

Point Predictive Releases Q2 2026 Fraud Risk Intelligence Report

Credit Union Collection Professionals Announces 2027 CUCP Summit in San Antonio, Texas