They’re Not Saving the Loan, They’re Only Delaying the Repo

–

Something has been holding repossession volumes down… but it’s not improving the borrower’s financial health.

Across the auto finance landscape, lenders have been leaning harder than ever on loan modifications, extensions, deferrals, and re-aging strategies, to manage rising delinquency levels. On the surface, this has helped prevent a sharper spike in repossessions. Underneath, however, a more complex and potentially dangerous trend is forming, one that directly impacts borrowers, lenders and recovery agents alike.

Two Markets, Two Strategies

Not all lenders are responding to high auto loan delinquency the same way.

Captive finance companies, the lending arms of automakers, have used modifications conservatively. Their borrower base is stronger, their collateral newer, and their loss tolerance lower. Estimated modification activity typically falls in the low single digits, even during stress cycles.

By contrast, subprime and alternative-finance lenders are operating in a different reality. With materially higher delinquency rates, these lenders appear to be using modifications as a core servicing strategy, not a last resort.

- Subprime 60+ day delinquencies have hovered around 6%+ in recent data

- Prime delinquencies remain below 1%

That gap explains everything.

For subprime lenders, modifications are not just about helping borrowers, they are about slowing the pace of loss recognition.

No Transparency

Outside of Asset Backed Securities (ABS), where investors are allowed full access to data sets, there is virtually no product level data made available on historic loan modification volume or trends.

But we do have that data available. What it does show:

- 90%+ of loan modifications are extensions

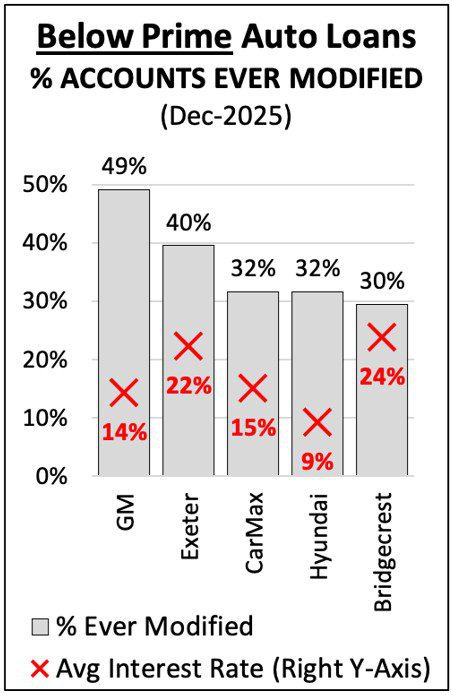

- 49% of all GM financed ABS loans have had at least one modification

- Exeter, 40%, CarMax, Hyundai 32%, Bridgecrest 30%.

- Of all ABS loans 11+ days delinquent, 32% have been modified at least once by YE 25’

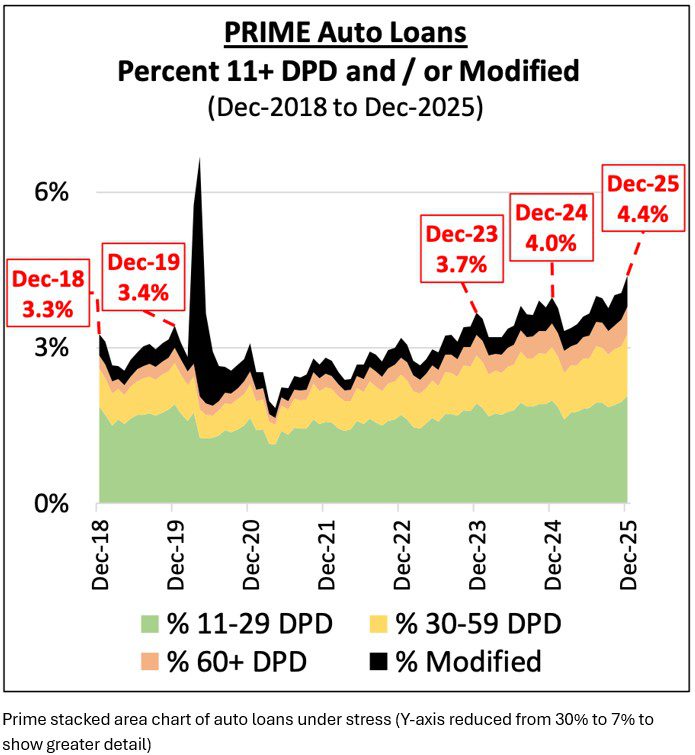

- ABS loan modifications have increased over 6% since before the pandemic.

It is clear; many lenders are giving away loan modifications and extensions like candy.

In the credit union and bank spaces, most are doing the same.

In addition, most do not count loan extensions as loan modifications. This results in an undercounting of the impact of loan extensions.

Often forgotten or ignored with loan modifications or extensions is that the extended payment and earned interest don’t just go away, they reduce loan to value and increase losses when finally repossessed.

The Illusion of Stability

From the outside, repossession volumes have not always matched the level of borrower distress. That disconnect has led to confusion across the industry.

But the explanation is increasingly clear:

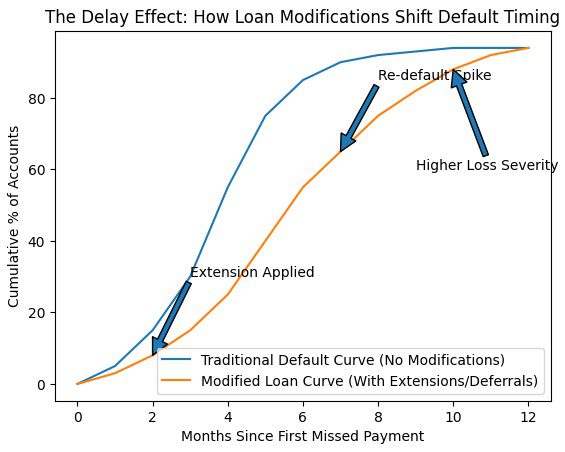

Loan modifications are acting as a pressure valve, delaying repossessions, not eliminating them.

Extensions push payments out. Deferrals pause them. Re-aging resets delinquency clocks. All of it buys time.

For lenders, that time can be used to:

- Avoid immediate charge-offs

- Improve short-term portfolio performance metrics

- Delay costly recovery and remarketing processes

–

But time does not fix affordability.

The Delay Effect

At first glance, the numbers appear contradictory:

- Delinquencies are elevated

- Repossession rates are rising

- Charge-offs remain high

Under normal conditions, those three metrics would move in a tighter sequence. Instead, they are happening simultaneously.

That only works if something is interrupting the natural progression of default.

That “something” is loan modification.

The LTV Problem No One Is Talking About

Here’s where the situation becomes more serious, and where the long-term risk is building.

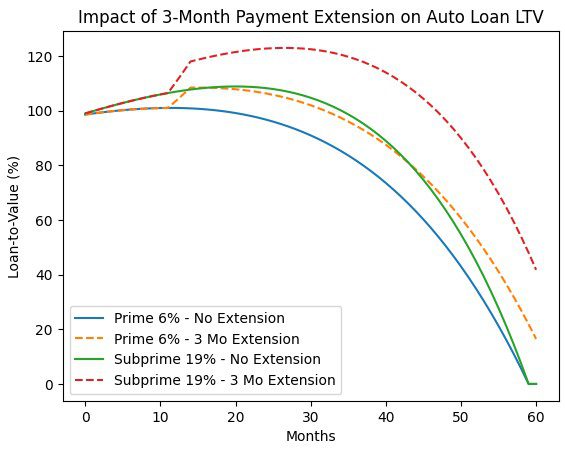

When a loan is modified, the balance rarely decreases meaningfully, but the clock keeps ticking on depreciation.

Deferment impact on LTV.

- LTV increases immediately during the extension period

→ No principal reduction while the car continues depreciating - Subprime loans (19%) show significantly worse LTV deterioration

→ Higher interest = slower principal paydown = deeper negative equity - The impact is permanent

→ Even after payments resume, the loan never “catches up” to its original LTV path

That creates a dangerous dynamic:

- Vehicle values continue to fall

- Loan balances remain elevated

- Negative equity deepens

–

This is classic LTV (Loan-to-Value) deterioration, and modifications accelerate it.

In many cases:

- A borrower who was slightly upside-down on their loan becomes deeply negative

- A recoverable asset becomes a loss-heavy liquidation

- A borderline account becomes economically unviable to repossess early

In effect, modifications can turn:

A manageable loss today into a significantly larger loss tomorrow.

Why This Matters for Repossession Agents

For recovery agents, this shift is already being felt, even if it’s not always obvious.

1. Delayed Assignments

Accounts that would have hit placement earlier are being held longer. This creates:

- Gaps in volume

- Less predictable assignment flow

- Vehicles are harder to locate and recover

2. Worse Condition Collateral

By the time repossessions occur:

- Vehicles are older

- Mileage is higher

- Condition is often worse

3. Higher Charge-Off Pressure

Lenders facing larger losses may:

- Push harder on suppressing fees

- Scrutinize invoices more aggressively

- Delay or slow walk payments

When Modifications Meet Reality

The biggest risk isn’t the modification itself, it’s what happens when it fails.

And many do.

Industry data strongly suggests that a large percentage of seriously delinquent loans eventually charge off, even after intervention. When that happens, the system doesn’t absorb the loss gradually, it absorbs it all at once.

That’s when:

- Repossession volumes surge

- Recovery pipelines flood

- Servicers tighten controls

The Link to Lender Failures

Now connect this to what the industry has already seen.

Recent lender collapses, including high-profile failures in the subprime and alternative-finance space, follow a familiar pattern:

- Rising delinquencies

- Increased reliance on modifications

- Delayed loss recognition

- Cash flow strain

- Eventual collapse or servicing transfer

When lenders fail, the consequences extend beyond their balance sheets.

Recovery agents have already experienced:

- Unpaid invoices

- Frozen receivables

- Assignments transferred without legacy obligations honored

In cases like Tricolor and Automotive Credit Corporation, far too many agencies found themselves just another debt in large pools of unsecured creditors unlikely to ever get paid.

What Comes Next

If current trends continue, the industry is likely heading toward a delayed correction, not an avoided one.

Expect:

- Continued reliance on modifications in 2026

- Gradual increase in repossession volume as re-defaults hit

- More volatility in assignment flow

- Ongoing financial stress among weaker lenders

Final Thought

Historically, Examiners discouraged the heavy use of loan extensions and modifications.

Why? because they didn’t want lenders trying to hide delinquency or “Roll” it as they used to say.

Why? Because the “extend and pretend” strategy masks the true state of a portfolios weaknesses.

This can lead to the failure of finacial organizations with little adequate warning to investors, borrowers or vendors.

Unfortunately, in the aftermath of the Great Recession, political pressure made Federal Examiners relent in their negative view of modifications. Worse, the pandemic encouraged them.

And here we are.

Loan modifications are not inherently bad. In many cases, they are the right call, for both borrower and lender.

But the question remains:

At what point does helping a loan survive simply make the eventual failure worse?

Because often what is being delayed today is only going to be worse in the future.

–

Kevin Armstrong

Publisher

Loan Modifications – The Illusion of Stability Suppressing Repossession Volume – Loan Modifications – The Illusion of Stability Suppressing Repossession Volume – Loan Modifications – The Illusion of Stability Suppressing Repossession Volume

Loan Modifications – The Illusion of Stability Suppressing Repossession Volume – Repossession – Repossess – Repossession – Lending – Subprime Auto Loans – Subprime Auto Loans – Auto Loan – Delinquency – Credit Union Collections – Credit Union Collectors – Lending – Auto Loan

More Stories

The Dealer You Never Underwrote

Army Enlistment Papers, Fake Credit Union Loans, and a Vegas Getaway

The Psychology of Fraud: Where Fear, Greed, and Opportunity Collide

United Creditors Connect 2026 Brings All-Star Speaker Lineup to Las Vegas

CRS 2026 Recap: Delinquencies, Operational Strain, and the AI Turning Point

Auto Delinquencies Show Mixed Signals in April