Fewer Institutions. Smaller Auto Portfolios. Smarter, Harder Collections.

–

For decades, credit union collections operated on a familiar model: steady volumes, predictable delinquency cycles, and a largely manual approach to borrower engagement. That model is now under pressure from multiple directions at once.

The number of credit unions is shrinking. Auto loan portfolios, the backbone of many collections departments, are no longer reliably expanding. And emerging forces like artificial intelligence and outsourced servicing are redefining how collections work gets done.

What’s emerging is not a decline in collections, but a fundamental restructuring of the function itself.

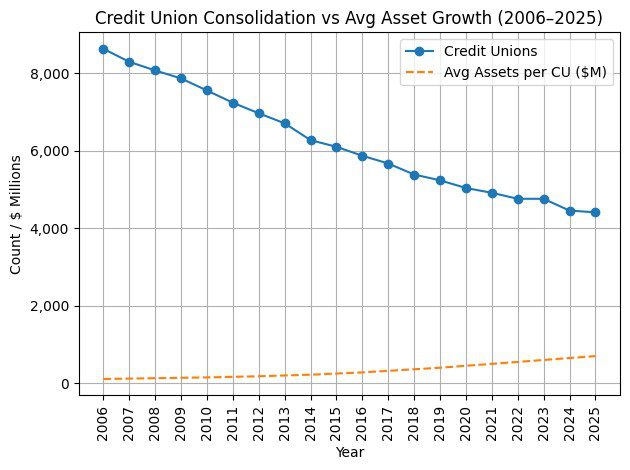

A Smaller Industry with Larger Stakes

The consolidation trend is undeniable.

- In 2010, there were over 7,300 federally insured credit unions

- By 2024, that number had fallen to 4,499

- By the end of 2025, it dropped further to approximately 4,287 (CUSO Magazine ®)

This is not a temporary contraction, it is a long-term structural shift driven by mergers, succession challenges, and the inability of smaller institutions to keep up with regulatory and technological demands (NCUA).

For collections, the implication is clear:

Fewer credit unions, but each one carries larger, more complex portfolios and higher performance expectations.

Collections is no longer a back-office function. It is becoming a strategic lever tied directly to financial performance.

The Auto Loan Plateau, and Why It Matters

For years, auto lending has been the engine behind credit union loan growth, and by extension, collections activity.

That engine is now showing signs of slowing.

- Credit unions held roughly $486 billion in auto loans as of late 2025,

- But balances declined year-over-year and quarter-over-quarter (CUTimes)

At the same time:

- Loan growth overall has slowed to just 0.3% median growth in 2025 (NCUA)

- Smaller credit unions are seeing loan declines and membership erosion simultaneously (Tyfone)

This shift matters because collections has historically relied on:

- High-volume, secured loan portfolios

- Predictable recovery cycles

- Consistent replenishment of delinquent accounts

That environment is changing.

The future collections pipeline will be less about volume, and more about precision and efficiency.

The End of Traditional Collections Methods

Legacy collections strategies are increasingly misaligned with today’s environment.

Historically, collections departments relied on:

- Static call queues

- Broad segmentation (prime vs. subprime)

- Manual workflows and collector discretion

- Limited data beyond payment history

These methods were effective in a world of:

- Growing portfolios

- Lower compliance scrutiny

- Less borrower communication complexity

Today, they are becoming liabilities.

Why?

Because modern portfolios demand:

- Faster intervention

- More accurate risk identification

- Consistent, documented borrower engagement

And traditional methods simply cannot scale to meet those expectations.

AI Is Not a Tool, It’s a Structural Disruptor

Artificial intelligence is rapidly moving from experimental to essential.

Credit unions are beginning to deploy AI in collections to:

- Predict delinquency before it occurs

- Segment borrowers by behavioral risk, not just credit score

- Optimize contact timing and channel selection

- Automate routine communication and follow-up

This fundamentally changes how collections operates.

Instead of reacting to delinquency at 30 or 60 days, AI enables:

Pre-delinquency intervention, often before the account is even past due

The result:

- Higher cure rates

- Lower cost-to-collect

- Reduced reliance on manual processes

But it also creates a new challenge:

Collections teams must now compete with algorithms that are faster, more consistent, and increasingly more accurate.

Outsourcing Is Accelerating, But Not Without Risk

At the same time, many credit unions, particularly those growing through mergers, are turning to outsourced collections solutions.

The drivers are clear:

- Talent shortages

- Rising compliance complexity

- Technology investment costs

- Need for scalability

Outsourcing offers:

- Immediate operational capacity

- Access to advanced technology platforms

- Standardized processes

But it also introduces tension. Credit unions must balance:

- Efficiency vs. control

- Cost savings vs. member experience

- Scale vs. personalization

In a member-driven model, collections cannot become purely transactional.

The institutions that succeed will be those that integrate outsourcing without losing oversight, data visibility, or member alignment.

Compliance Is Raising the Floor for Everyone

Regulatory expectations continue to rise, particularly around:

- Communication practices

- Documentation and auditability

- Consumer protection standards

This disproportionately impacts:

- Smaller credit unions

- Manual collections environments

- Inconsistent processes

As a result, collections operations are being forced to:

- Standardize workflows

- Document every interaction

- Align with enterprise-level compliance frameworks

This is another driver pushing the industry toward:

- Technology adoption

- Centralization

- Professionalization

The New Collections Model: Smaller, Smarter, Integrated

All of these forces, consolidation, slowing loan growth, AI, outsourcing, and compliance, are converging into a new model for credit union collections.

That model looks fundamentally different:

From Volume → Precision

Fewer accounts, but greater focus on outcomes

From Reactive → Predictive

Intervening before delinquency, not after

From Manual → Automated

Systems guiding strategy, not just supporting it

From Isolated → Integrated

Collections aligned with lending, risk, and member experience

The Bottom Line

The future of credit union collections is not defined by decline, it is defined by evolution under pressure.

The industry is moving toward:

A smaller, more consolidated ecosystem where collections is data-driven, technology-enabled, and strategically integrated into the full credit lifecycle.

The institutions that adapt will not just collect more effectively, they will:

- Reduce losses earlier

- Strengthen member relationships

- Improve overall portfolio performance

Those that do not will find themselves operating with:

- Outdated methods

- Higher costs

- Increasing competitive disadvantage

Because in this new environment, collections is no longer just about managing delinquency.

It is about managing risk, relationships, and outcomes, simultaneously.

–

Kevin Armstrong

Publisher

Half the Credit Unions, Double the Pressure: The New Reality of Collections – Half the Credit Unions, Double the Pressure: The New Reality of Collections – Half the Credit Unions, Double the Pressure: The New Reality of Collections

Half the Credit Unions, Double the Pressure: The New Reality of Collections – Credit Union Collections – Credit Union Collectors – Lending – Delinquency – Auto Loan – NCUA – NCUA –

More Stories

Are Auto Loan Delinquencies Getting You Down?

Auto Finance Fraud Poised to Surpass $10 Billion in 2026

Auto Finance Risk Series: A Structural Shift in Credit, Collateral, and Recovery