On Today’s Agenda! – Again

Sacramento, CA – 15 June, 2020 – The results of a vote this week could very well be one of the final steps taken to cripple the California lending market for years to come. AB 2501, the disastrous “Job Killer Bill”, providing no questions asked forbearances until the year 2023 and forcing judicial only repossessions and foreclosures, has until Friday the 19th to pass the state Assembly and is scheduled for a floor vote today. Aside from it’s insane June 11th revisions, the bill appears to have been designated a “Suspense Bill” which would close down any open debate on the Assembly floor.

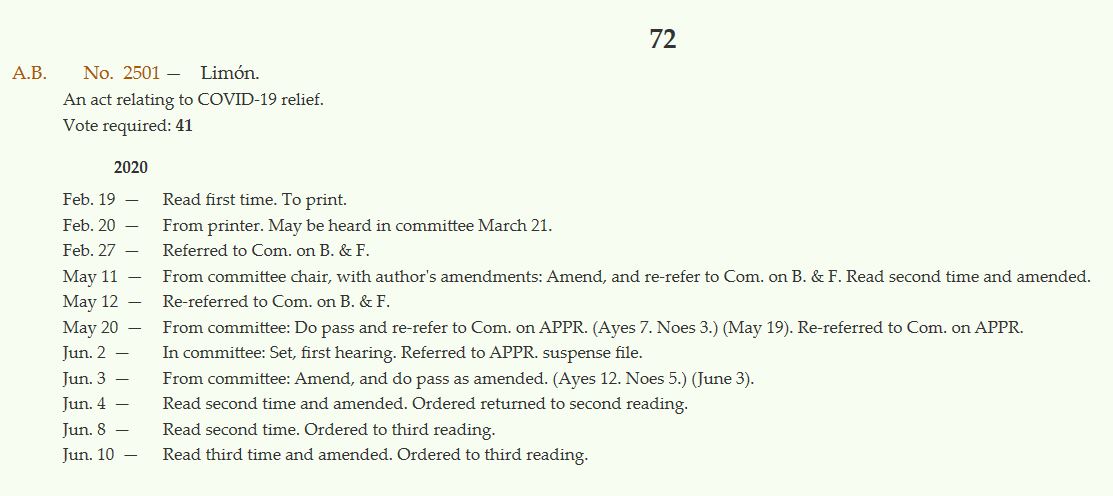

The California State Assembly posted their schedule for bills to come to vote and AB 2501 appeared as item number 72. Whether or not it makes it to vote today or the day after is unknown, but it is on today’s calendar scheduled to open at 1pm, PST. Fair warning, these hearings are audio only and heavily redacted in broadcast. They’re a little camera shy and, based upon their recent passing of ACA 25, seem to prefer to operating in private.

The full assembly meeting can be listened to live, here

Bill Status

Many in the credit union world had hoped, and almost expected, to see major revisions to the bill somewhere along the way, including the hope of a carve out for credit unions. This has not transpired and the bill has actually tightened its language and closed the original open-ended and state of emergency period based term, which is now extended to January 1, 2023.

Yes, January 1, 2023. It’s not a typo as many had thought. It’s written into the bill three times.

Regarding the status, if it is indeed a “Suspense File”, according to the state assembly website;

“Suspense File bills are then considered at one hearing after the state budget has been prepared and the committee has a better sense of available revenue. No testimony is presented – author or witness – at the Suspense File hearing.”

The bill, removed from the floor on Thursday the 11th at the last minute, was apparently placed in a “Suspense File” status, which does not show on the bill’s status on the state’s website, but which I had heard said by the Assembly chair and also heard through an industry lobbyist. If this is correct, there will be no open debate on the bill when it hits the floor and will receive only a simple up or down vote.

This bill has no state budget expenses that I can think of, nor mentioned, and other than the dramatic loss of tax revenue the state would suffer, the conversion to a “Suspense File” status appears strategic. It’s author appears to be uncomfortable debating this publicly.

The state budget deadline is June 15th. The deadline for a vote on this bill is June 19th. This date range is consistent with what had been suggested by two sources as the probable window for a vote.

This bill has already passed two committees, one of which was the very one headed by the bill’s author, Assembly Woman Limón, the Assembly Banking and Finance Committee and the second, the Appropriations Committee. Combined, the bill received 17 aye, 6 noes and 3 not present votes. These are unique votes in that several of the committee members were on both committees. These members also vote in the full assembly and will likely vote consistent to their previous votes.

The California State Assembly has eighty seats currently filled with 61 Democrats (76.3%), 17 Republicans (22.5%) and 1 Independent (1.3%). In order to pass, AB 2501 must only achieve a simple majority of 41. Assuming that all of the committee members that votes “Aye” do so again, only 24 new votes out of the 44 remaining. A mere 55%.

Having sat through a couple of these Assembly hearings, I can attest that the sentiment and reasoning of the vast majority of this body are led by emotion and anything with the word “Covid-19” on it stands a very strong chance of getting rubber stamped for approval. This bill’s passage in the Assembly appears inevitable.

The Bill’s Author

I do not intend to be insulting or critical of Assembly Woman Limón. I have never met her. I only know what I can find online about her and believe that she believes that what she is doing is in the best interest of the citizens of the state of California. But what I can’t understand is why she is the chair of the Assembly Banking and Finance Committee? What were her qualifications?

According to her Assembly biography and Wikipedia, her sole work experiences comprise of a seat on the local school board for ten years and the educational sector. With only one year in the office as an Assembly person, she was appointed the chair seat of the banking and finance committee, where she has been since 2017. Assembly Woman Limón graduated with a BS from UC Berkeley and a Masters from Columbia University in unknown majors. Based on her post-graduate activities, it would be safe to assume they are educational focused.

With her lack of experience in office at the time of her chair appointment and apparent lack of any experience in the financial services sector, it is curious that she was placed in the position of the Assembly Banking and Finance Committee of the largest state in the Union and fifth largest economy in the world.

The Bill’s Origins

AB 2501 is strikingly similar to two bills brought before congress, Financial Services Committee Chairwoman, CA Rep. Maxine Waters’ H.R. 6379, the “Take Responsibility for Workers and Families Act and Ohio Senator Sherrod Brown’s S. 3565. Both died on the vine with 6379 being attached to the doomed “Heroes Act” and Brown’s bill never reaching the floor for vote.

On a national scale, these were easily seen for the long-term damage they can do to our nation’s financial health and had no chance of passage. Here in California, with a super-super majority in both houses and the governor’s office, the opportunity to pass this is almost bullet proof.

Opposition

AB 2501, titled “the COVID-19: homeowner, tenant, and consumer relief Law of 2020” , has been opposed by every major bank, credit union, finance and auto sales association in the state and has thus far been able to move through the first two lower committees with relative ease.

The California Credit Union League, a long-time beneficiary and supporter of the state’s Democratic Party, has rolled out massive grass roots efforts to defeat this bill. From CEO’s all the way down to tellers, credit union staff have been reaching out to the state Assemblypersons to express their concerns over this “Job Killer” bill just over the last few days.

The bill, introduced on May 11th, is receiving heavy opposition from the California Chamber of Commerce, American Bankers Association (ABA), American Financial Services Association (AFSA), Bank Policy Institute (BPI), Credit Union National Association (CUNA), Housing Policy Council (HPC), Mortgage Bankers Association (MBA) and the Securities Industry and Financial Markets Association (SIFMA.)

On the May 17th, joint letter from the California Chamber of Commerce, American Bankers Association (ABA), American Financial Services Association (AFSA), Bank Policy Institute (BPI), Credit Union National Association (CUNA), Housing Policy Council (HPC), Mortgage Bankers Association (MBA) and the Securities Industry and Financial Markets Association (SIFMA), it was stated that;

“AB 2501 would undermine these ongoing efforts to help customers by creating duplicative and sometimes contradictory requirements for the mortgage and auto finance industries when viewed alongside federal rules, regulations and program requirements established by Congress, regulatory bodies, federal executive agencies, and government sponsored enterprises.”

In a more direct letter, the California Chamber of Commerce referred to the bill as “JOB KILLER” and that “Requiring these institutions to potentially go years without receiving payment is a significant burden that will negatively impact financial opportunities for Californians. Given the financial risk this proposal creates for such institutions, there is no question that the institutions will limit the mortgage and auto loans it offers. There will likely be stricter criteria to qualify, or, higher rates to offset the potential loss these institutions could suffer under AB 2501. This limitation will have a negative impact on the housing market, further exacerbating the housing crisis and creating job loss in the housing industry. It will also unquestionably limit car loans, especially for those with problematic credit history, and will harm both consumers and workers in the auto industry.”

Keep Up the Pressure!

If you have not done so already, please submit your “Connect for the Cause” message to your California State Assemblyperson regarding AB 2501 as soon as possible! We currently have just over 4,000 messages sent and need to reach 10,000.

Find Your Assembly Representative Here!

While the larger national and state financial associations have considerable clout, they do not represent the expressed interests of the repossession industry and your support of the California Association of Licensed Repossessors (CALR) lobby is still very much needed. Please donate today!