Record High Charge Off and Stubborn Delinquency Levels Set the Stage for a Rough 2026

–

Back in December when I reported out the 3rd quarter National Credit Union Administration’s (NCUA) 5300 FPR financials reports, I had made the suggestion that “perhaps the worst of the delinquency is over.” Boy was I wrong.

Keeping everything in perspective, the fourth quarter is traditionally the period of the highest delinquency and charge off. So, it is no surprise that Q4 of 2025 was high. But with credit union auto loan portfolios running off quicker than they can be funded, the ratios are really working against the industry.

Download the Data Here!

–

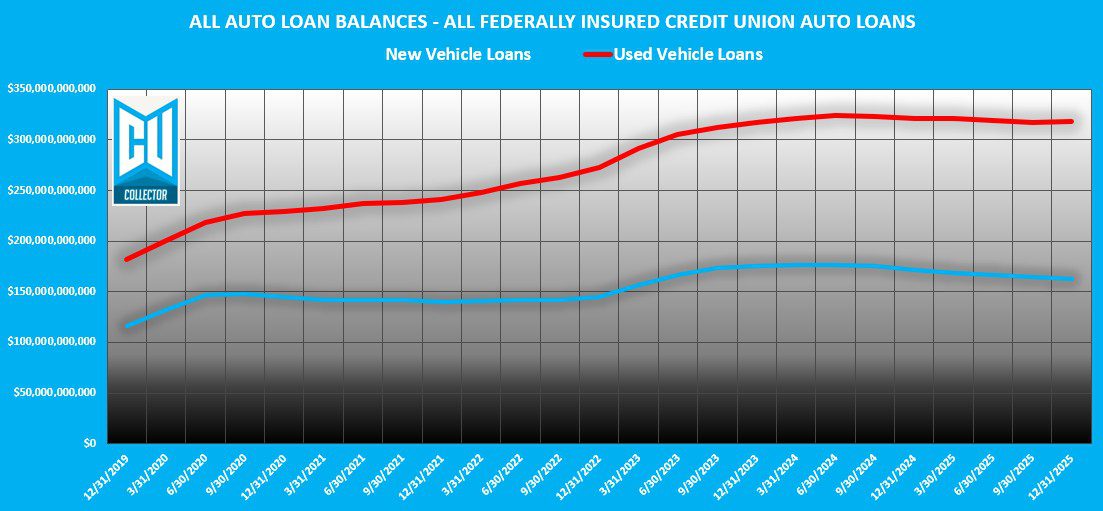

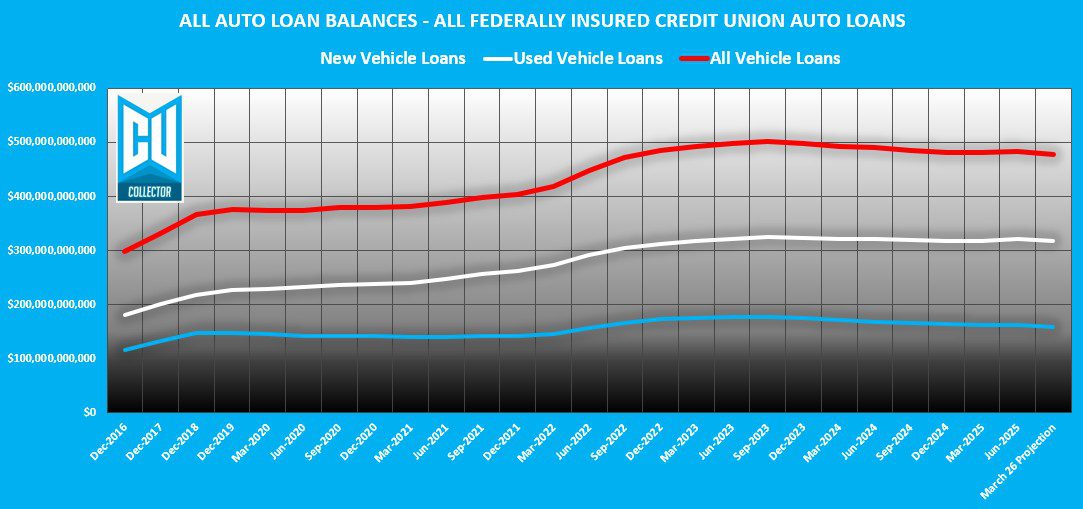

Portfolio Balances: Running Off Persists

Q4 was a bloodbath for credit union auto loan portfolios. Back at the Q3 report I had predicted some continued runoff of an additional $184M and a year-end balance of $481.2B. What actually happened made me triple check the data.

Combined, new and used, credit union auto loan portfolios finished at $480.1B. That was $2.2B in loan balance reductions in Q4 alone. Comparing it to Q4 of 2024, it was an overall $1.4B lower marking the lowest auto loan portfolio balances since Q3 of 2022.

My Q3 predictions overall were so off, I’m not sure I even trust my own predictions but, I am afraid its only going to get worse in Q1 of 2026 with an additional $2.2B in runoff.

–

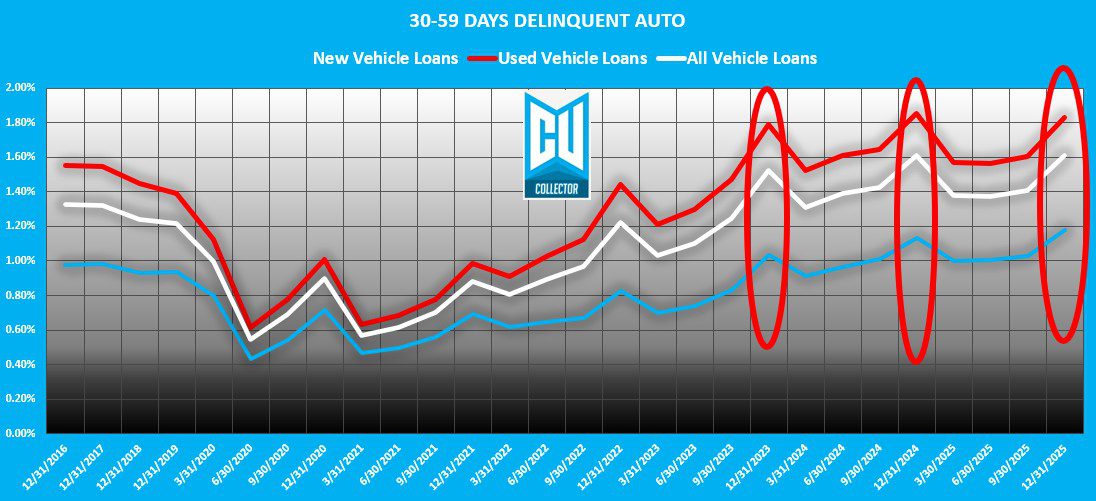

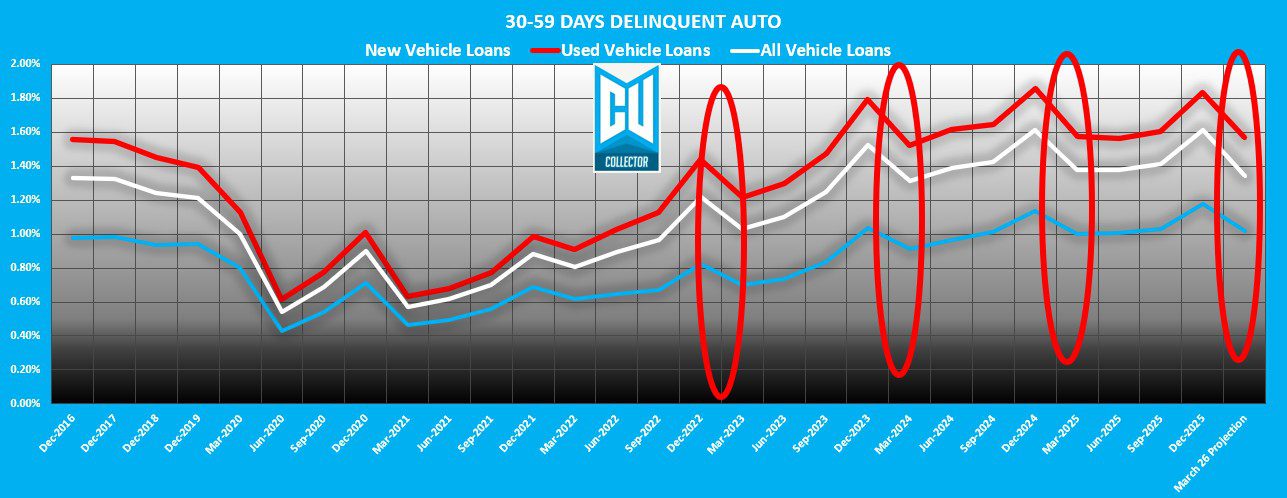

30-Day Delinquencies: History Repeating

I had expected an increase in early-stage delinquency (30-59 days) and wasn’t surprised. While I had predicted that Q4 would finish at $7.4B, I wasn’t far off.

Q4’s 30-day delinquency finished at $7.7B. Just $5M lower than Q4 of 2024. This trend sends a strong signal that 2026 could turn out to be a re-run of 2024.

Looking at all trends, Q1 tends to show some relief as tax refunds start rolling in, but under the current spike in oil and gas prices, it will likely be a little more muted. My model suggests Q1 will end at $6.4B, but I’m not buying it.

–

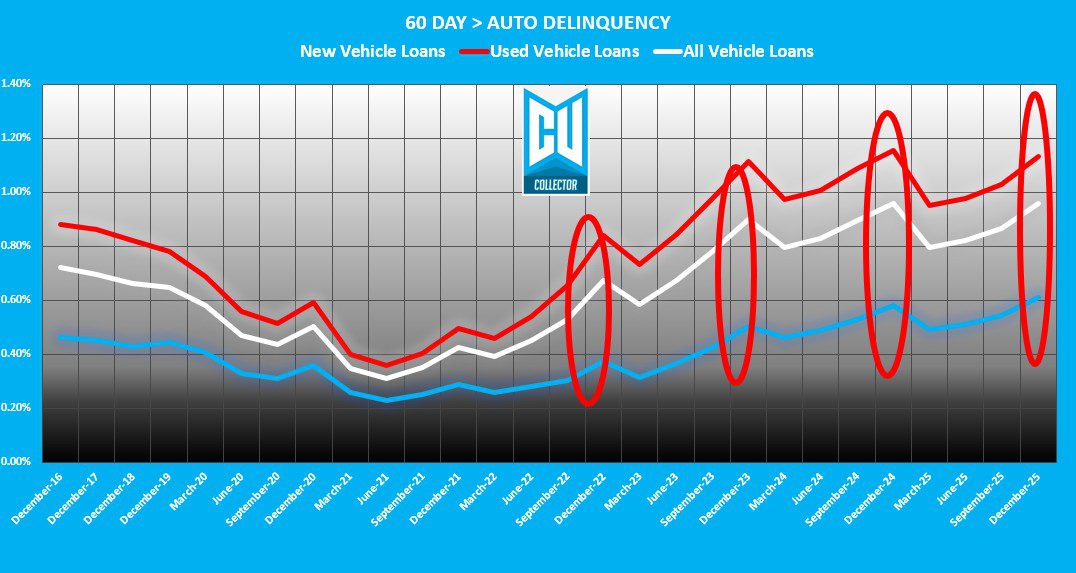

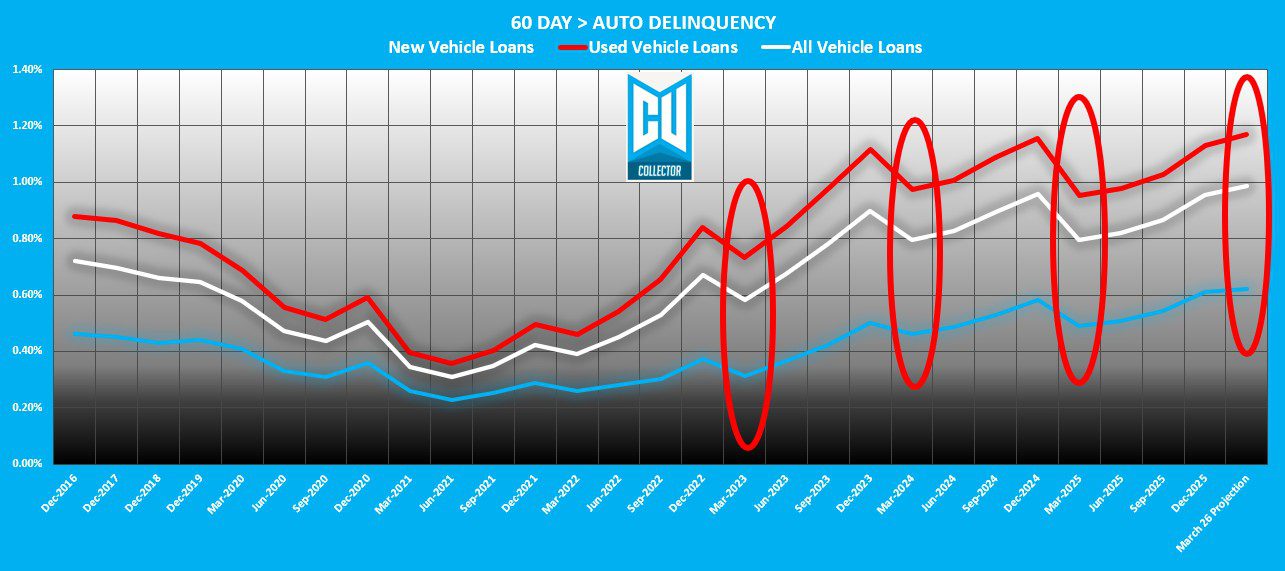

60+ Day Delinquencies: Reportable

As expected, Q4 reportable delinquency (60 days and up) showed a large increase. With a $942M increase in the 60-89 day category alone, it grew by a total of $414M.

This was actually better than I had expected. I had suspected it to increase to $4.8B with a delinquency ratio of 1.01%. Finishing at $4.59M with a 0.96% ratio, it was almost a mirror of Q4 2024.

As previously mentioned, I fear that Q1, which traditionally is the lowest delinquency rate quarter of the year, will not provide the expected reductions everyone might want. My trends model suggests that Q1 will end at $3.9B. While this is some welcome relief, keep in mind, Q1 of 2025 finished at $3.8B. If the rest of the year comes out the same, we can expect 2026 to hold steady or perhaps from a ratio standpoint, worse than 2025 mostly due to shrinking auto loan portfolios driving up the ratios even when the numeric value is the same or lower..

–

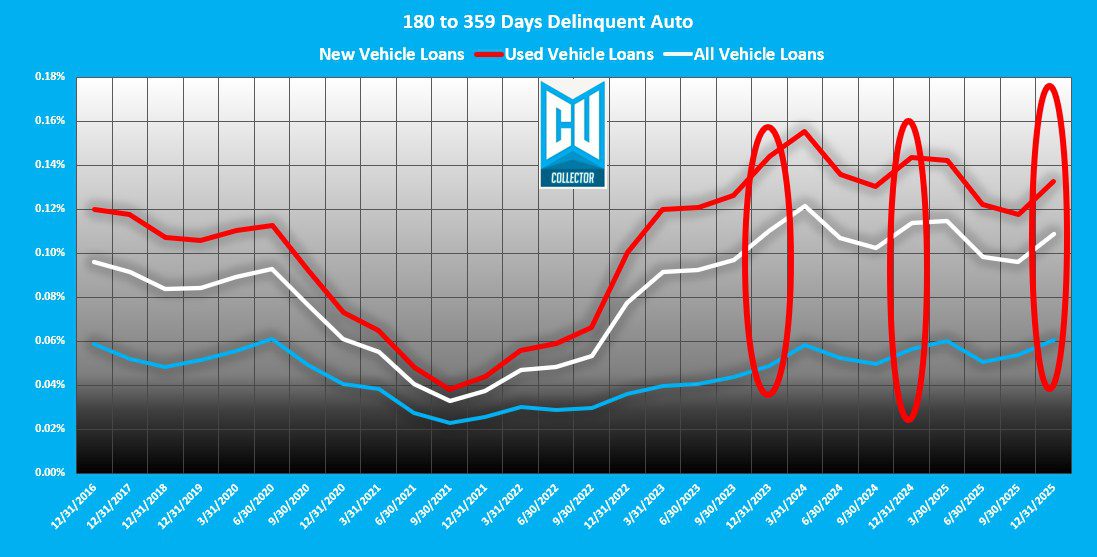

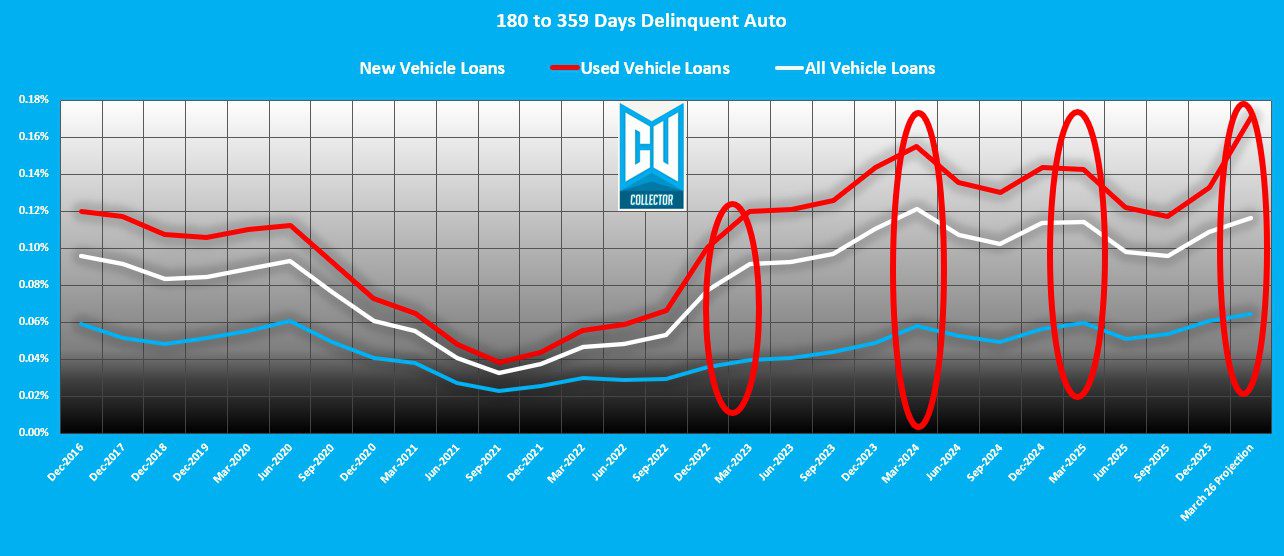

180+ Days Delinquent: The Bone Yard

Repossessions, bankruptcies and deficiency balances. There’s not usually much meat left on the bones in this queue. And as expected, it rose again.

I had predicted a year end finish of $511M and wasn’t far off with a year end total of $521M. Had the next topic not have been so consequential, this category and reportable delinquencies would have been far worse.

–

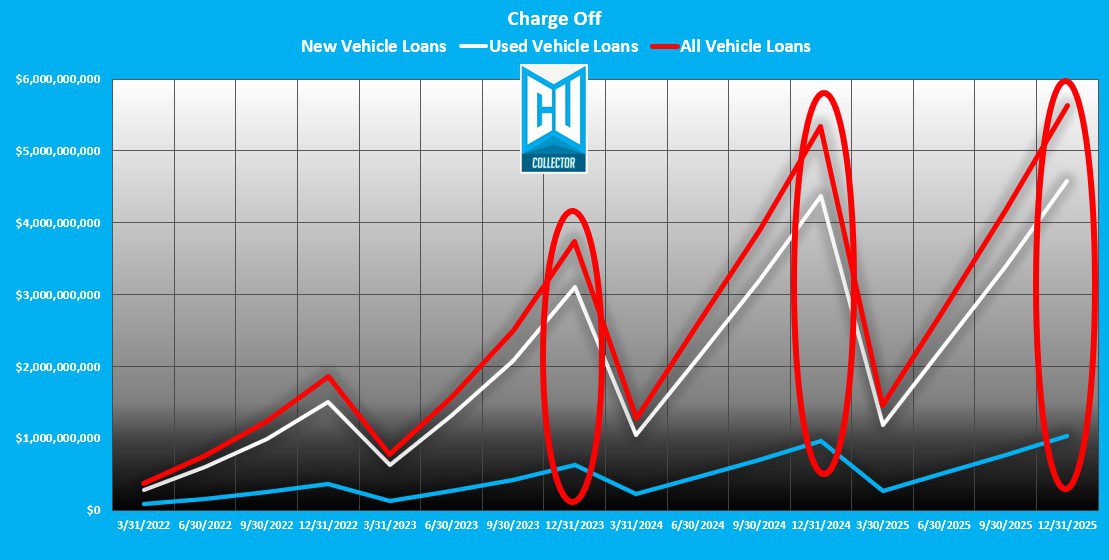

Charge-Offs: The Final Flush

Credit unions were pretty aggressive in their charge offs for year end. I had expected a year end aggregate total of $4.7B which would have been a reduction of $628M over 2024. But what happened I did not expect.

Total gross charge offs for credit union auto loans finished at a whopping $5.6B. That’s $291M higher than in 2024. Had this not happened we doubtlessly would have seen the highest reportable auto loan delinquency in available NCUA data going back to 2016.

–

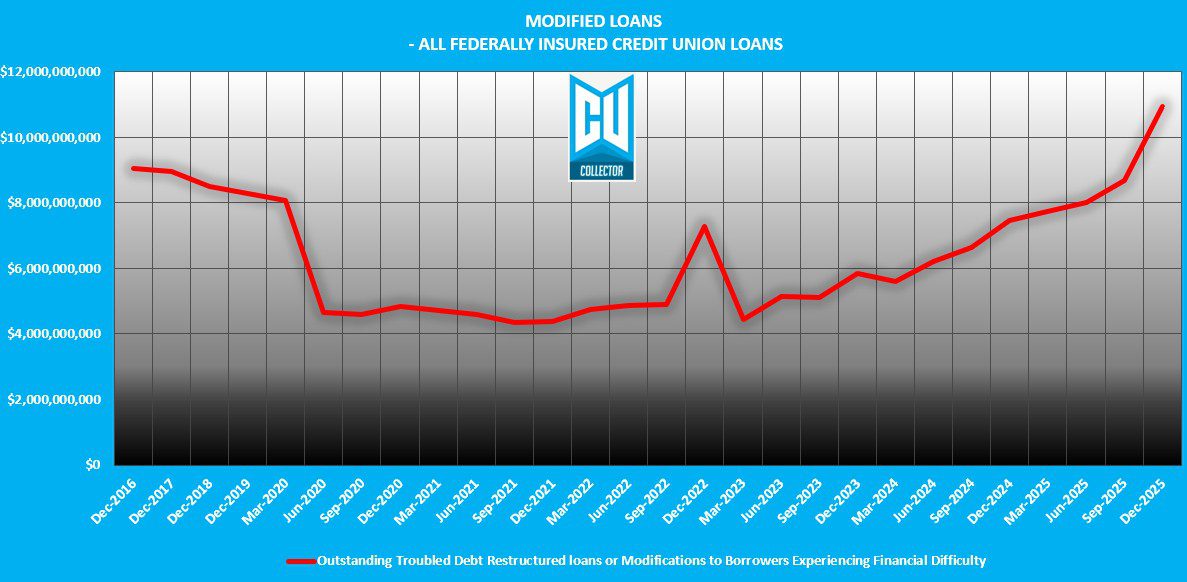

Loan Modifications: Record Highs

Is it me or do Loan modifications just seem to be out of control? December showed a total of $10.9B in modified loans.

Keep in mind, the reported data does not count simple loan extensions and does not break down this category by loan product, but it is the highest known level of loan modifications since at least 2016 when the NCUA began these aggregate reports.

This is either symptomatic of an economy seriously stressed to the breaking point or a credit union industry that is actually reporting these impaired loans as they should have been all along. Something that I know for years most credit unions weren’t doing consistently.

–

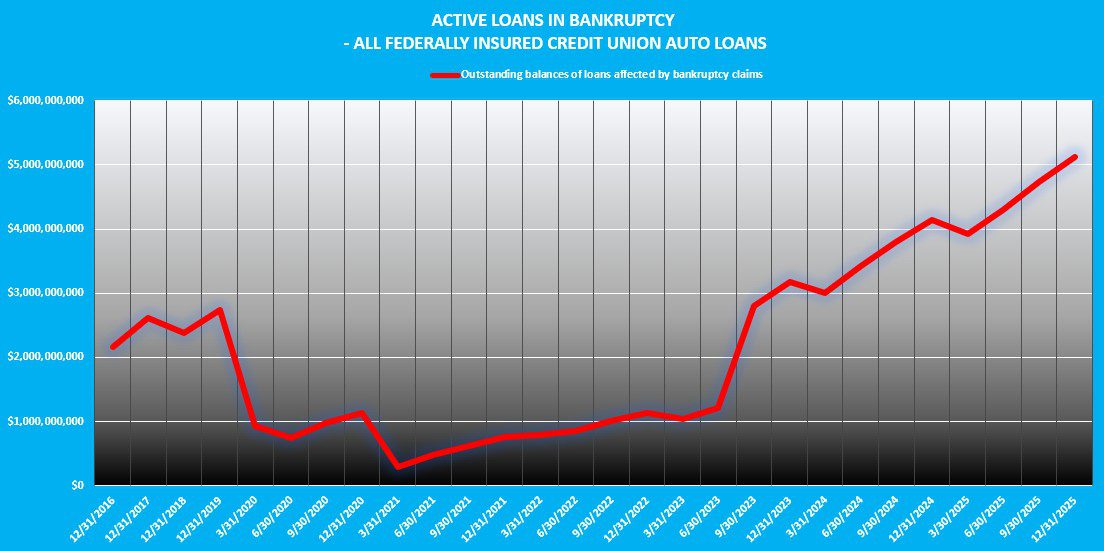

Bankruptcies – The Rising Tide

This is another category that the NCUA reports without breaking it down to the loan product level. While $5.1B in loan bankruptcy balances is high, we do not know how many of these are corporate level bankruptcies which have been in a slow and steady rise since the pandemic.

Download the Data Here!

Summary

I don’t think that war in Iran and skyrocketing gas prices were on anyone’s bingo cards for 2026, but here we are. Judging by what we know already, unless new loan originations bounce back and the economy stabilizes soon, I believe we have strong reason to believe that 2026 is going to at very least be another rough year. I just pray that I am wrong.

Kevin Armstrong

Publisher

–

Related Articles;

Q3 2025 Credit Union Auto Loan Delinquency – Light at the End of the Tunnel?

Q2 2025 Credit Union Auto Loan Delinquency – A Slow but Rising Tide

Q1 2025 Credit Union Auto Loan Delinquency – Buckle Up Buttercup

The Calm Before the Storm – 1st Quarter 24’ Credit Union Auto Loan Delinquency

Credit Union Auto Loan Delinquency Climb Continues

Credit Union Auto Loan Delinquency Surges

Credit Union Auto Loan Delinquency Pattern Back to Normal

Q4 2025 Credit Union Auto Loan Delinquency – An End of Year Meltdown – Q4 2025 Credit Union Auto Loan Delinquency – An End of Year Meltdown – Q4 2025 Credit Union Auto Loan Delinquency – An End of Year Meltdown

Q4 2025 Credit Union Auto Loan Delinquency – An End of Year Meltdown – Credit Union Collections – Credit Union Collectors – Lending – Auto Loan – NCUA – NCUA – Delinquency – Repossession – Repossess – Bankruptcy

More Stories

Identity Vampires Prey on Vulnerable Elders

Auto Loan Delinquencies Edge Lower in February 2026

Free Webinar: How Credit Unions Can Modernize Operations with the Right Tech Partner