–

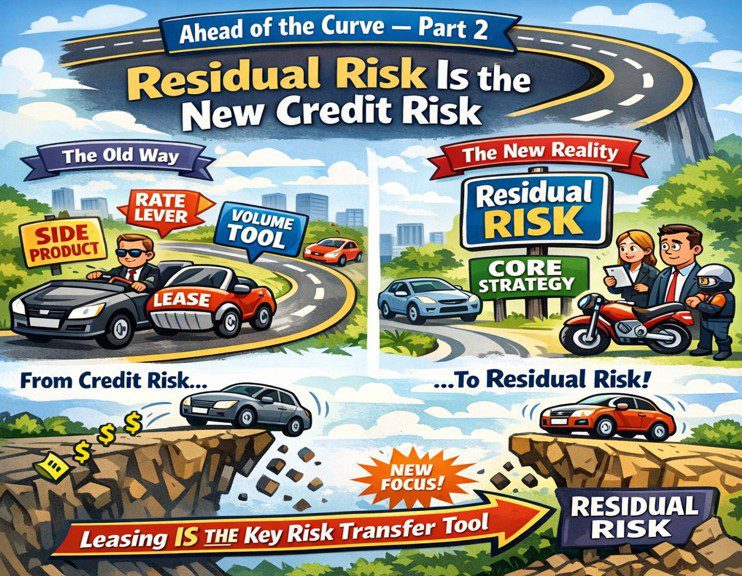

One of the biggest risks in Auto Finance isn’t Credit anymore… it’s Residuals. And most organizations aren’t structured for that shift.

For years, the industry treated Leasing like a sidecar product… a rate lever, a volume tool, a way to smooth monthly payments when retail financing hit its limits.

That era is over.

Today, leasing isn’t “back.” It’s becoming the most important risk‑transfer instrument.

Not about promotional payments… it’s about residual exposure becoming the new credit exposure.

- Leasing isn’t returning –> it’s transforming

The lenders who think leasing is simply recovering from a down cycle are missing the point.

Leasing is evolving into the primary mechanism for:

• Absorbing asset value volatility

• Controlling downstream loss severity

• Managing capital partner expectations

• Reshaping portfolio duration and risk mix

Retail loans push risk forward.

Leases contain it.

- Everyone sees EV Volatility… almost no one sees the deeper shift.

EV Residual Swings are the headline.

But the real story is broader:

• ICE depreciation curves are destabilizing

• Repair inflation is pushing more units into total loss territory

• Insurance premiums are distorting affordability

• OEM pricing strategies are breaking historical residual models

The result: Residual risk is now behaving like credit risk… unpredictable, asymmetric, and portfolio defining.

Underwriting can’t solve that.

Residual strategy can.

3.) The next competitive war won’t be fought in underwriting.

Underwriting is becoming commoditized:

• Same Bureaus

• Same Models

• Same data

• Same constraints

• Increasing regulatory pressure limiting differentiation

The real differentiation is shifting to:

• Residual forecasting

• Remarketing velocity

• Grounding discipline

• Portfolio level asset management

• Capital partner alignment on loss timing and severity

• Dynamic pricing tied to real-time asset performance

• Tighter integration between originations & remarketing functions

Pure retail portfolios are becoming structurally exposed. The next wave of lenders will operate blended architectures… using leases to absorb asset volatility and ABS loans to drive volume, yield, and capital efficiency. The advantage won’t come from choosing one or the other, but from designing a portfolio that can flex with market conditions.

The lenders who win the next cycle won’t have the best credit box, they’ll have the best asset‑value strategy.

This shift isn’t theoretical because it’s already showing up in loss curves, lease pricing, and capital conversations.

The question isn’t whether Residual Risk will dominate… it’s whether your organization is structured to manage it.

Residuals used to be an actuarial exercise. Now they’re a source of strategic leverage, and only a few lenders know how to use it.

–

Part 3 of the “AoC” series drops next.

–

Servicing Solutions – VP, Loss Mitigation | Auto, Lease & Powersport Finance | Risk & Recovery Strategy | LGD, Remarketing & Portfolio Performance

–

–

–

Related:

Ahead of the Curve: Part 1 – Payment Elasticity is the Real Constraint

Ahead of the Curve — Part 2 – Residual Risk Is the New Credit Risk – Ahead of the Curve — Part 2 – Residual Risk Is the New Credit Risk – Ahead of the Curve — Part 2 – Residual Risk Is the New Credit Risk

Ahead of the Curve — Part 2 – Residual Risk Is the New Credit Risk – Delinquency – Bankruptcy – Lending – Auto Loan – Credit Union Collections – Credit Union Collectors – Repossession – Repossess – Repossession – Remarketing

More Stories

Did the CFPB Accidentally Create the Credit Washing Industry?

The New Face of Auto Loan Fraud: When AI Becomes the Borrower’s Co-Signer

When a Loan Funds a Scam: Who Bears the Loss?

Stop Wrongful Repossessions Before They Start

Why the Hallway Conversations May Be the Most Valuable Part of UCC 2026

The Clock Is Ticking on CCUCC’s Early Registration Cash Giveaway