Auto Finance isn’t constrained by rates anymore. It’s constrained by Math.

–

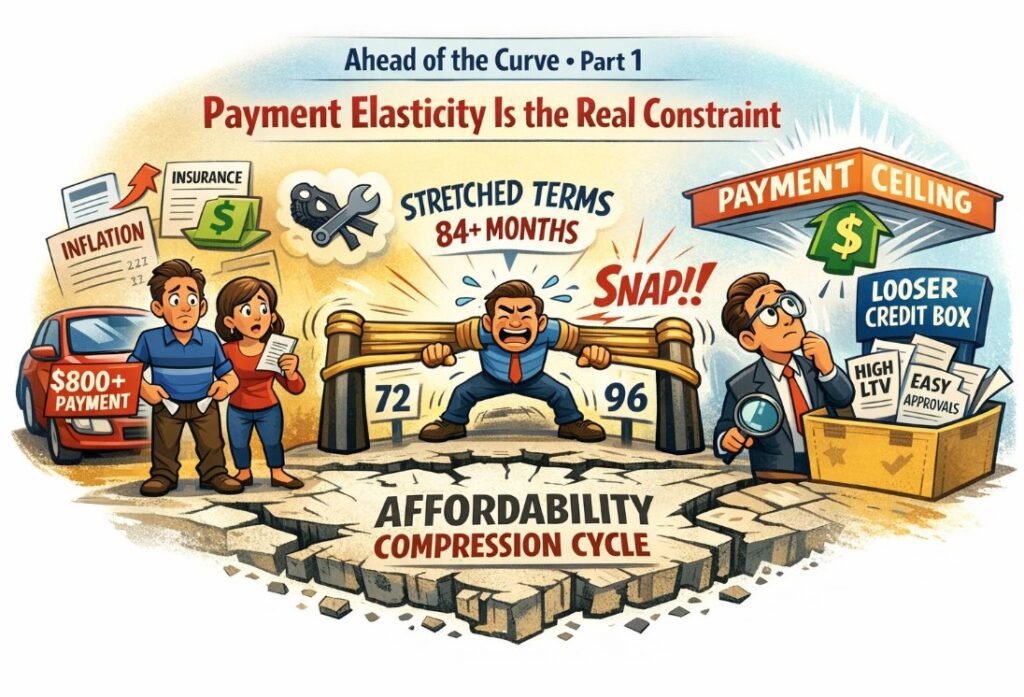

The industry keeps obsessing over rates and 60+ DPD delinquencies. The real constraint, the one reshaping everything… is Payment Elasticity.

Payment Elasticity = the point at which higher payments no longer produce demand, regardless of credit availability.

Consumers have hit the mathematical limit of what they can pay.

If you’re still framing 2024–2026 as a “rate cycle,” you’re already behind. This is an Affordability Compression Cycle, and it’s far more structural.

1. Payments have outpaced income growth for half a decade.

This is the part the headlines miss.

• New car payments >$800 are now normal

• ~15–20% of new buyers are in $1,000+ payments (vs. low single digits pre‑2020)

• Insurance inflation is compounding the problem

• Maintenance + Repair costs are rising faster than wages

• Even prime borrowers are stretching beyond comfort

• Median income growth has lagged payment growth by ~20–30 pts since 2019

This isn’t a temporary squeeze. It’s a structural affordability reset.

2. Term Extensions have reached their limit

For years, lenders solved affordability by stretching terms. But now:

• 72–84 months is standard

• 96 months is creeping in –> effectively “lifetime financing” on a depreciating asset

• Negative equity rollovers are compounding

• Payment‑focused underwriting is masking true risk

We’re out of runway. You can’t stretch a term that’s already stretched.

3. The Credit Box + Term Extension model is breaking

Quietly, lenders are loosening:

• Higher LTVs

• Softer stips

• More exceptions

• Greater tolerance for weaker credit

Not because they want to, but because origination flow has to continue.

This isn’t tactical drift. It’s the early stage of a structural shift.

4. The industry is approaching a Payment Ceiling, not a Rate Ceiling

Even if rates drop, affordability doesn’t reset.

• Vehicle prices are structurally higher

• Insurance is structurally higher

• Maintenance is structurally higher

Delinquencies are a lagging indicator. Payment Elasticity is a leading one.

We’re not in a Rate Cycle. We’re in an Affordability Compression Cycle, and it’s redefining the economics of ownership.

EXECUTIVE IMPLICATION

Pricing won’t solve this. Product design will.

The next competitive advantage is Redefining Ownership Economics:

• Subscription models

• Flexible lease structures

• Usage‑based financing

• Hybrid access models

• Asset‑light mobility structures

The lenders who understand the math — not just the rates — won’t just survive the next cycle; they’ll define the next business model and own the next decade.

–

Part 2 of the “AoC” series drops next.

If this perspective adds value to your work:

🔖 Save for your next Strategy, Risk, or Portfolio Review

🔵 Connect/Follow Lance Harp for continued analysis across Auto, Lease, & Powersport Finance

–

Servicing Solutions – VP, Loss Mitigation | Auto, Lease & Powersport Finance | Risk & Recovery Strategy | LGD, Remarketing & Portfolio Performance

–

–

Related:

Series Intro —> “AHEAD OF THE CURVE: The Structural Shifts Reshaping Auto, Lease & Powersports Finance”

Ahead of the Curve: Part 1 – Payment Elasticity is the Real Constraint – Ahead of the Curve: Part 1 – Payment Elasticity is the Real Constraint – Ahead of the Curve: Part 1 – Payment Elasticity is the Real Constraint

Ahead of the Curve: Part 1 – Payment Elasticity is the Real Constraint – Delinquency – Bankruptcy – Lending – Auto Loan – Credit Union Collections – Credit Union Collectors – Repossession – Repossess – Repossession – Remarketing

More Stories

A Different Kind of Money Laundry

Federal Banking Agencies Issue New Guidance on Immigration-Related Credit Risk

The Auto Finance Paradox

Early Bird Registration for CCUCC 2026 Ends August 14

Credit Union Collection Professionals Announces 2027 CUCP Summit in San Antonio, Texas

Closing the 30-Day Blind Spot: How Lenders Can Shut Down Auto Loan Bust-Out Fraud