Q1’s Brief Seasonal Dip in Delinquency Sets the Stage for Another Rough Year in Auto Delinquency

–

With holiday season behind us and tax refunds streaming in, Q1 offered its usual respite from the peak delinquency numbers. But, Q2, almost completely behind us, is shaping up to be a return to 2025’s numbers.

No one would have forecasted a war in Iran and records high gas prices into the 2026 economic forecast, but here we are. As if this wasn’t hard enough on everyone, interest rates are still stubbornly high and credit union auto loan originations continue to run off faster than they get funded.

Download the Data Here!

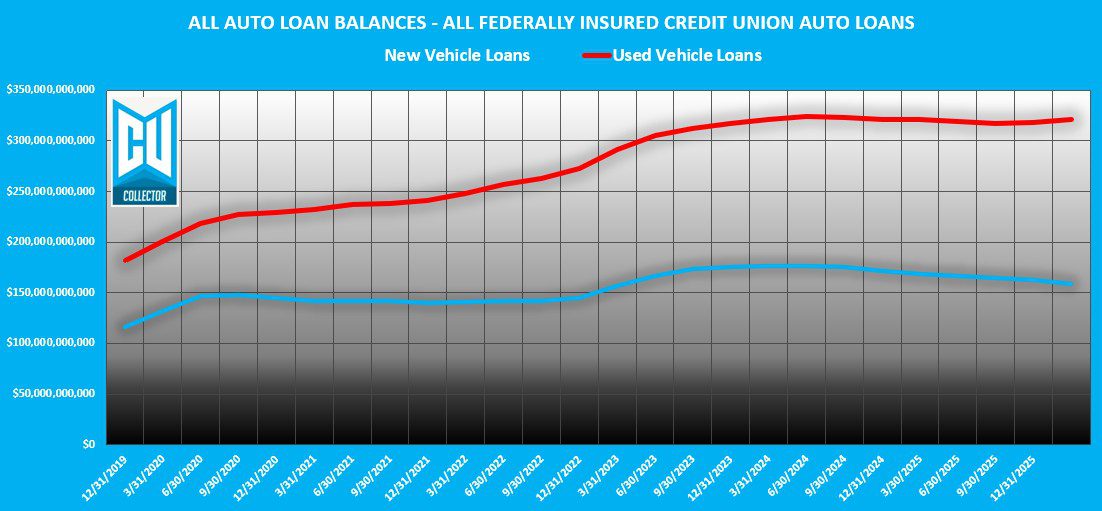

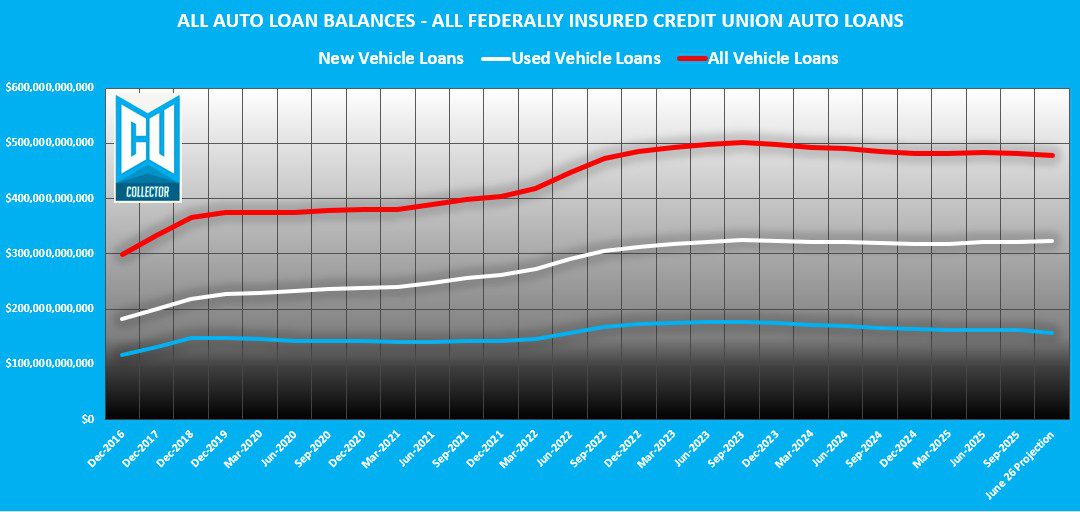

Portfolio Balances: Running On Empty

As previously stated, Q4 was a bloodbath for credit union auto loan portfolios. Q1 of 2026 was somewhat surprisingly more merciful.

In my Q1 2026 forecast, I had predicted it would be a $2.2B runoff. But as things turned out, it was the lowest reduction in loan balances since the slide began in 2023.

Combined, new and used, credit union auto loan portfolios finished at $479.5B. That was only a $514M in loan balance reductions. Comparing it to the heavy runoff we’d seen over the three years, it was something of a surprise.

My Q1 predictions were again way off. But I still suspect the runoff isn’t over. I project that Q2 will finish with another moderate runoff of $513M and hold balances just above $479B.

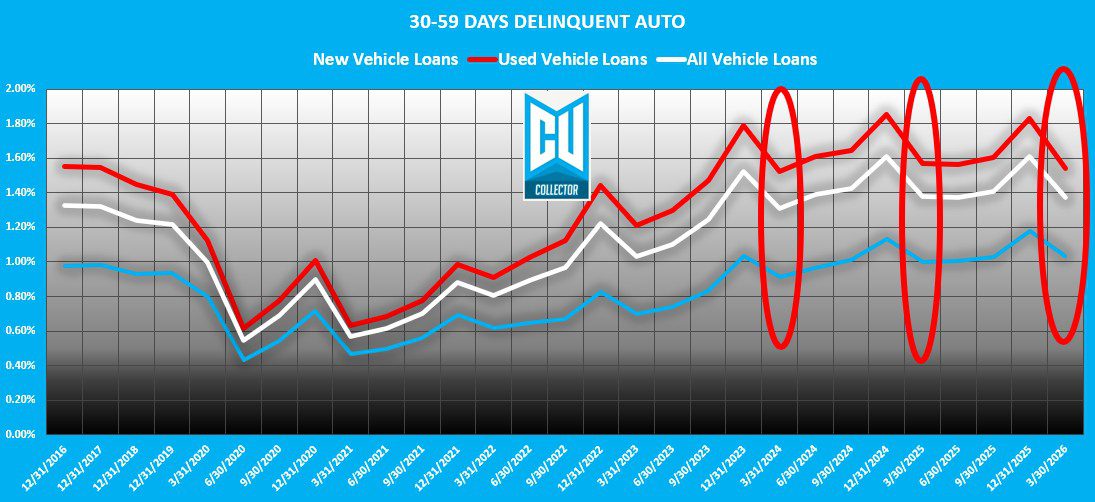

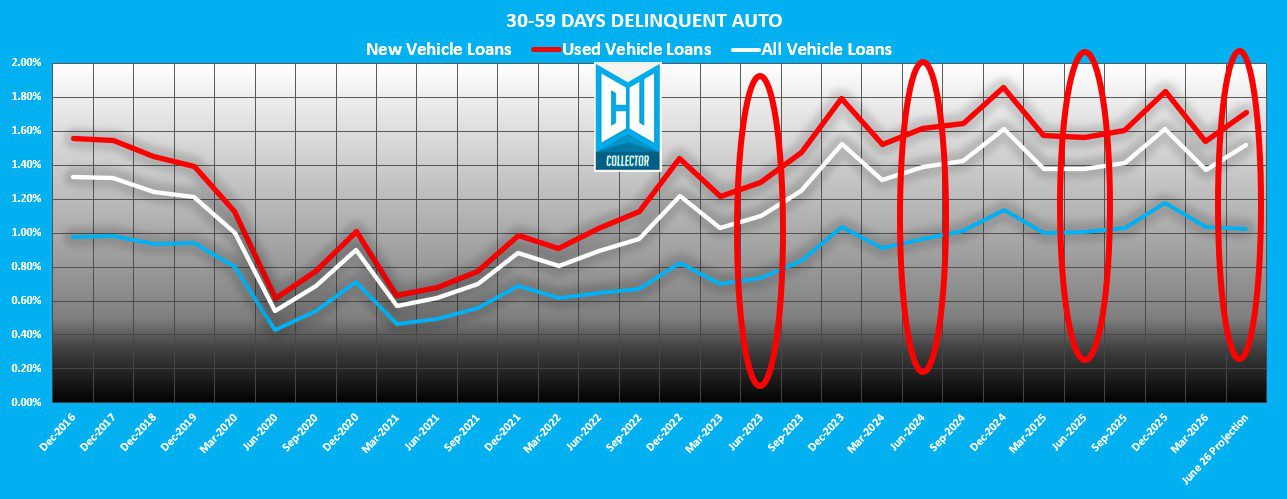

30-Day Delinquencies: Low But Higher

I had expected a decrease in early-stage delinquency (30-59 days) and wasn’t surprised with the results. I had predicted that Q1 would finish at $6.4B and wasn’t far off with a finish of $6.5B. This is was $1.1B lower than Q4 of 2025 and $58M lower than Q1 of 2025.

Q4’s 30-day delinquency finished at $7.7B. Just $5M lower than Q4 of 2024. This trend sends a strong signal that 2026 could turn out to be a re-run of 2024.

Unfortunately, my model suggests that Q2 will be a pretty big increase of $692M and finish at $7.2B.

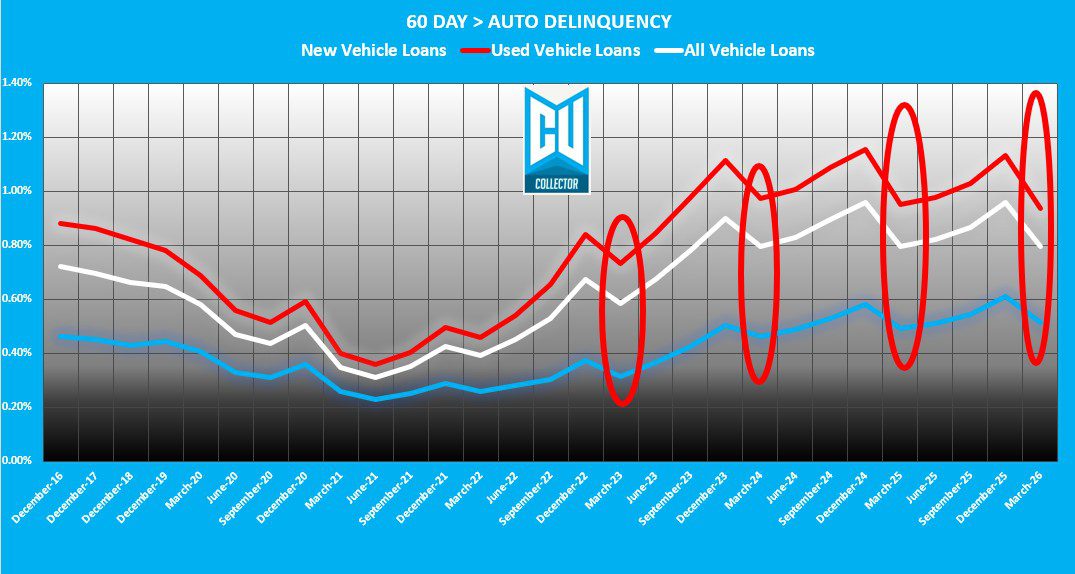

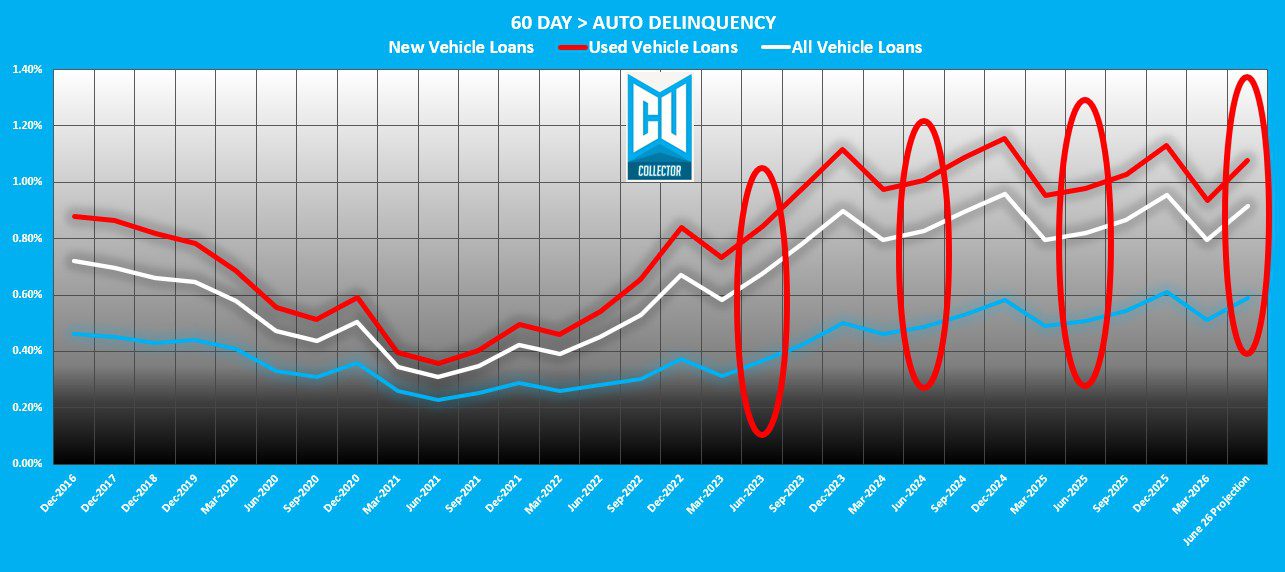

60+ Day Delinquencies: Reportable

As expected, Q1 reportable delinquency (60 days and up) showed a large decrease and finished at $3.8B. This was a mirror image of Q1 2025 both numerically and by its .80% delinquency ratio.

This was actually 0.02% and $124M better than predicted.

Seasonality has become largely predictable in the past few years and we can expect delinquency to start rising in Q2 and beyond. If all holds the same, we can expect a Q2 finish of $4.1B or 0.86%. This number is almost the same as 2025 but because of runoff, the ratio would finish at 0.86%.

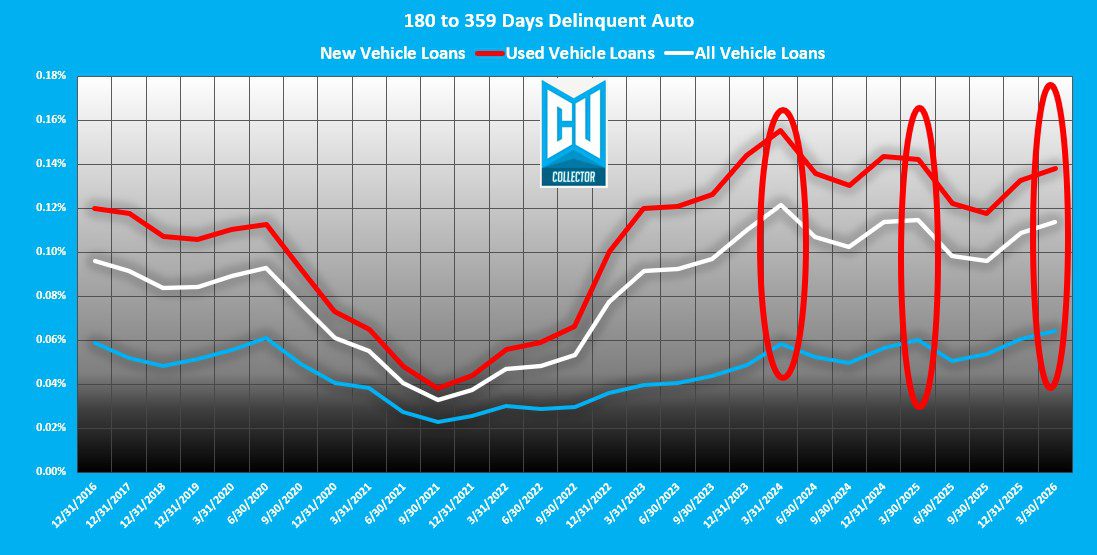

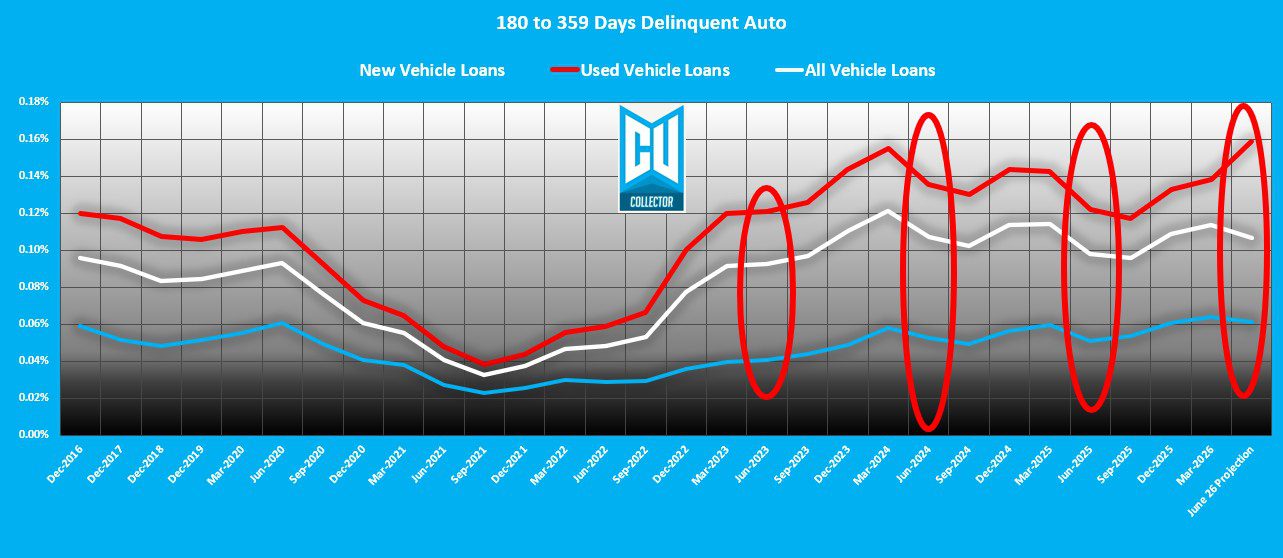

180+ Days Delinquent: The End of the Line

Other than repossessions, bankruptcies and deficiency balances, the 180+ day tranche of auto loans doesn’t usually hold much promise of anything more for reductions than charge off. And as usual, it rose.

I had predicted that Q1 would have finished at $556M. As it turns out, I was wrong again but we’ll see part of that reason why in the next section. While it finished at $544M and $11M lower than I had predicted, it was $69M lower than Q1 of 2025 which is an improvement.

I predict that we will see an additional reduction and finish the 180 day + bucket at $511M.

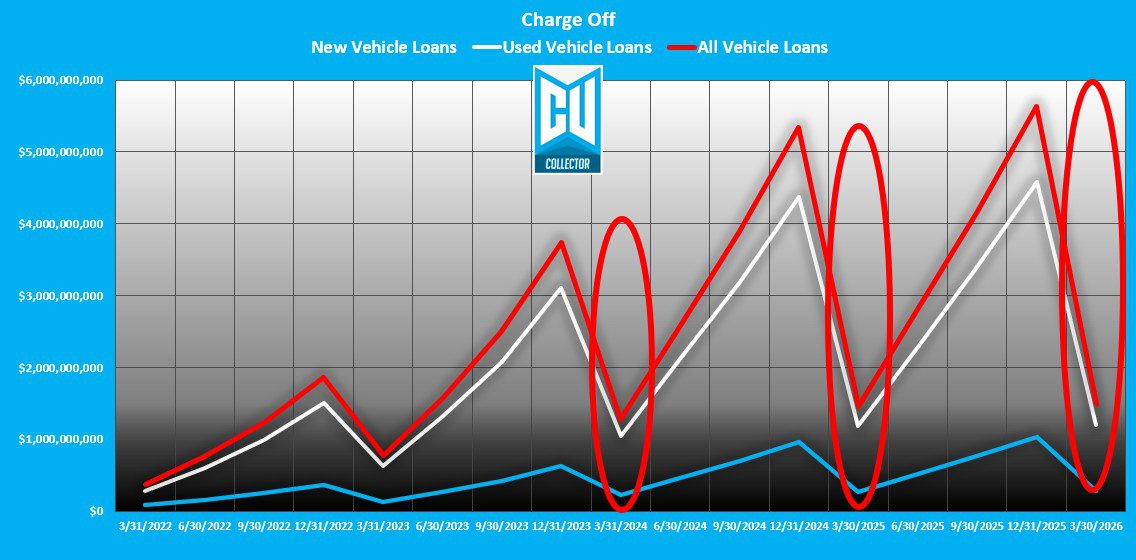

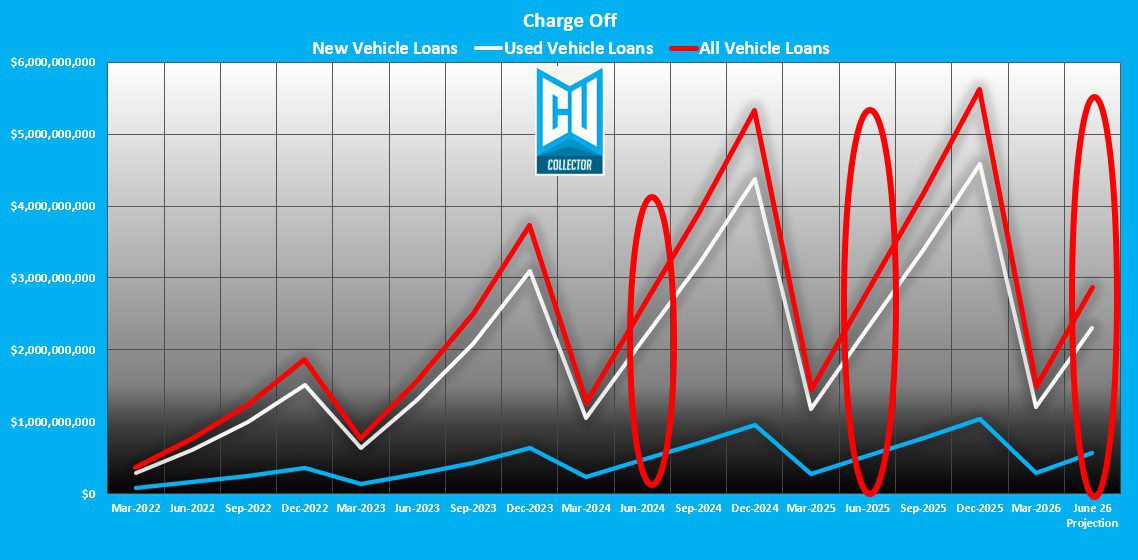

Charge-Offs: The Final Flush

What loans to refer for charge off and when can be pretty subjective, but it does show some indication on how aggressive credit unions choose to manage their loan portfolios. Judging from Q1’s charge off, it appears as though 2025’s tone and tenor are being maintained.

In Q1, credit unions charged off a total of $1.48B. That’s $319M more than I had predicted $1.1B, and $31M more than Q1 of 2025.

I project that we will continue to see robust charge-offs in 2026 and that Q2 will end at and aggregate $2.8B. That’s a quarterly increase of $1.4B and consistent with Q1 and Q2 of 2025. All together, 2026 is looking like it will finish close to 2025’s record high $5.6B

Loan Modifications: Record Highs

Loan modifications are simply out of control. While Q1 showed an aggregate balance reduction of $795M from Q4 2025’s record high of $109B, it still rests stubbornly high at $10.1B.

As I must again remind, the reported data does not count simple loan extensions and does not break down this category by loan product, but it is the highest known level of loan modifications since at least 2016 when the NCUA began these aggregate reports.

I hate to beat on my drum again, but loan modifications and extension may be kind, but they are band aids on bullet holes when it comes to managing delinquency. The net effect of loan mods and extensions is almost always paid for by collateral value depreciation as the borrower ends up paying more interest than principal in subsequent payments.

If you want to know more on my thoughts about this, please read my April l2026 article on the subject: Loan Modifications – The Illusion of Stability Suppressing Repossession Volume

I’m not even going to try to predict where this is going, but judging by the ABS subprime auto loan portfolios performances, I don’t believe it ends well.

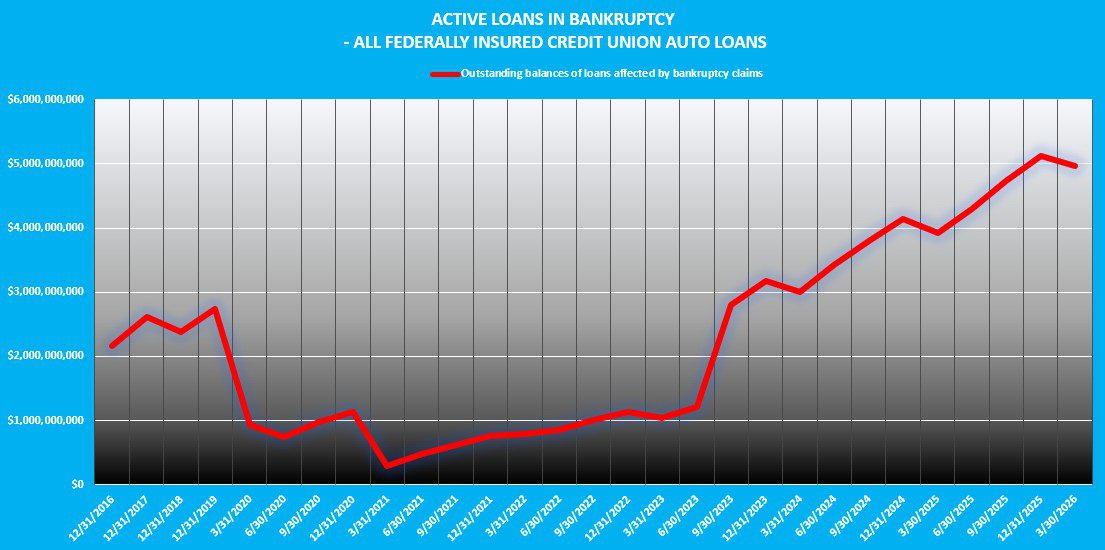

Bankruptcies – The Rising Tide

This is another category that the NCUA reports without breaking it down to the loan product level. In Q1 2026, the NCUA reported an aggregate of $4.9B in loan balances were in bankruptcy. This is actually a decrease of $157M.

Loan types matter significantly in this category because we do not know how many of these are corporate level bankruptcies or real estate secured which carry heavier balances and are not auto loans.

Either way, we have been watching a slow and steady rise since the pandemic.

Download the Data Here!

Summary

With the war in Iran in an on again and off again never-ending cycle that is keep fuel levels inflated, it is difficult to say of or when the economy will see any relief. But if the credit union share of auto loan originations continues at the current depleting levels and delinquency remains consistent, delinquency ratios will rise.

Overall, 2026 is already shaping up to be a mirror image of 2025 and looks like is going to be another rough year.

–

Kevin Armstrong

Publisher

–

–

Q1 2026 Credit Union Auto Loan Delinquency – Déjà Vu All Over Again – Q1 2026 Credit Union Auto Loan Delinquency – Déjà Vu All Over Again

Q1 2026 Credit Union Auto Loan Delinquency – Déjà Vu All Over Again – Credit Union Collections – Credit Union Collectors – Lending – Auto Loan – NCUA – NCUA – Delinquency – Repossession – Repossess – Bankruptcy

Related Articles;

Q4 2025 Credit Union Auto Loan Delinquency – An End of Year Meltdown

Q3 2025 Credit Union Auto Loan Delinquency – Light at the End of the Tunnel?

Q2 2025 Credit Union Auto Loan Delinquency – A Slow but Rising Tide

Q1 2025 Credit Union Auto Loan Delinquency – Buckle Up Buttercup

The Calm Before the Storm – 1st Quarter 24’ Credit Union Auto Loan Delinquency

Credit Union Auto Loan Delinquency Climb Continues

Credit Union Auto Loan Delinquency Surges

Credit Union Auto Loan Delinquency Pattern Back to Normal

More Stories

$95 Million Missing: Rolexes, Teslas, a Honduras Home, and a Credit Union CEO’s Fall From Grace

The Dealer You Never Underwrote

Army Enlistment Papers, Fake Credit Union Loans, and a Vegas Getaway

Identity Theft, Fake Pay Stubs, and Nearly $69,000 in Fraudulent Loans

Former Credit Union Loan Officer Admits Identity Theft in $100,000 Vehicle Fraud Scheme

The Psychology of Fraud: Where Fear, Greed, and Opportunity Collide