To see where this Auto cycle turns next, look at where Powersports is already bending.

–

If you’ve been in this industry long enough, you already know Powersports tends to move before Auto. But 2026 feels different. The signals coming out of Powersports right now aren’t just discretionary softness… they may be the clearest indicators yet of where the broader credit and asset value cycle is heading.

Three things are happening in Powersports that historically show up in Auto next.

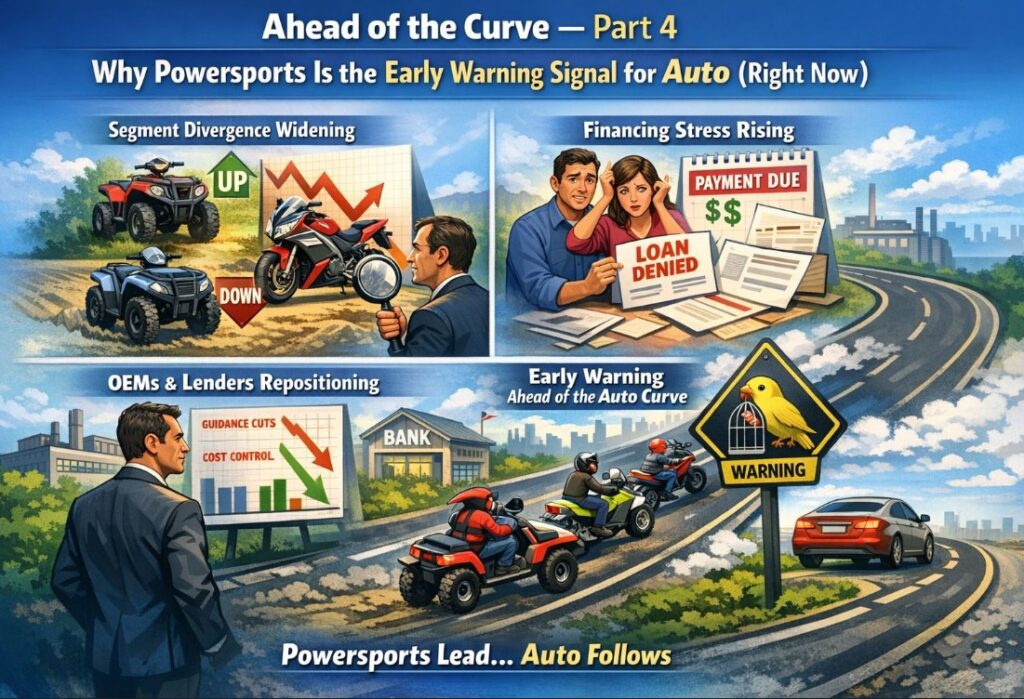

1. Segment Divergence Is Widening –> Earlier Than Usual

Recent market activity shows a growing split:

- Entry-level and utility units are holding up

- Higher-ticket recreational categories are softening

That divergence matters.

It’s one of the earliest signs of consumer trade-down behavior, & it typically surfaces in powersports before auto.

When buyers shift toward lower-ticket units in Powersports, Auto often follows with: - Lower trims

- Used over New

- Rising payment sensitivity

- Increasing incentive pressure

This is an early affordability signal.

2. Financing Stress Is Showing Up Faster in Powersports

Dealers are leading with financing earlier in the sales process… not because they want to, but because buyers are reaching payment thresholds sooner.

That’s the canary.

When financing becomes the constraint instead of the product itself, affordability pressure is already reshaping the buyer profile.

Why this matters:

Powersports portfolios tend to react faster to economic pressure because the collateral is more discretionary and the customer base is typically more payment sensitive.

We’re already seeing:

- higher payment sensitivity

- earlier credit friction

- more selective approvals

- lender caution on higher-ticket rec units

These are often the same signals that later emerge in auto… just on a lag.

3. OEMs and Lenders Are Repositioning Mid-Cycle

This may be the most important signal… and the one most people are missing.

Over the last several months, we’ve seen:

- OEMs becoming more conservative operationally

- Lenders shifting toward capital-light strategies

- Credit facilities extended to preserve liquidity

- F&I mix adjustments aimed at protecting margin

These are not purely growth-oriented moves. They are risk-management responses happening earlier in Powersports than in Auto.

When discretionary OEMs begin repositioning mid-cycle, it’s often because they’re already feeling:

- Margin compression

- Cost volatility

- Residual risk pressure

- Slower inventory turns

Auto tends to feel those same pressures later.

The Real Insight

Powersports isn’t just discretionary. It’s often where the cycle breaks first.

The industry often reveals changes in consumer affordability, credit appetite, & asset sensitivity earlier than almost anywhere else in vehicle finance.

–

–

Servicing Solutions – VP, Loss Mitigation | Auto, Lease & Powersport Finance | Risk & Recovery Strategy | LGD, Remarketing & Portfolio Performance

–

–

Related:

Ahead of the Curve — Part 2 – Residual Risk Is the New Credit Risk

Ahead of the Curve: Part 1 – Payment Elasticity is the Real Constraint

Servicing Is Eating Originations – Ahead of the Curve Part 3

Why Powersports Is the Early Warning Signal for Auto (Right Now) – Ahead of the Curve — Part 4 – Why Powersports Is the Early Warning Signal for Auto (Right Now) – Ahead of the Curve — Part 4 – Why Powersports Is the Early Warning Signal for Auto (Right Now) – Ahead of the Curve — Part 4

Why Powersports Is the Early Warning Signal for Auto (Right Now) – Ahead of the Curve — Part 4 – Delinquency – Bankruptcy – Lending – Auto Loan – Credit Union Collections – Credit Union Collectors – Repossession – Repossess – Repossession – Remarketing

More Stories

One Face. Sixteen Identities. $476,000 in Fraudulent Auto Loans

Did the CFPB Accidentally Create the Credit Washing Industry?

The New Face of Auto Loan Fraud: When AI Becomes the Borrower’s Co-Signer

Stop Wrongful Repossessions Before They Start

Why the Hallway Conversations May Be the Most Valuable Part of UCC 2026

The Clock Is Ticking on CCUCC’s Early Registration Cash Giveaway