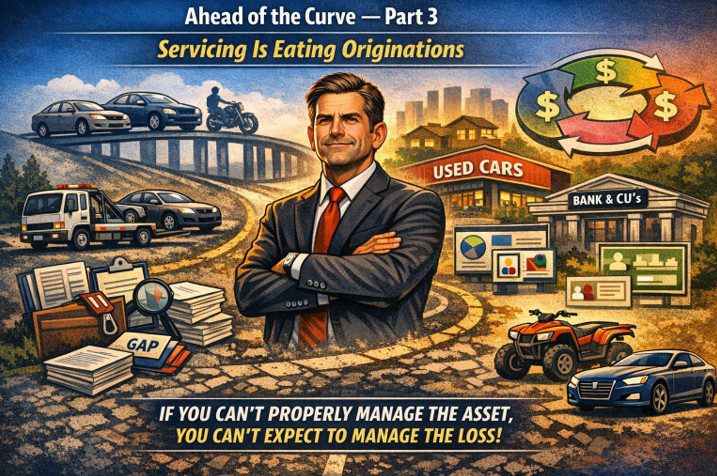

The lenders who build lifecycle ownership, not just origination, will own the next decade.

–

We’ve spent a decade optimizing originations. The real story now is what happens after the loan is booked… because Servicing is quietly eating the entire model.

For years, originations defined the industry… volume, pricing, credit box, advance.

But the center of gravity has shifted.

Servicing now defines profitability.

Not because originations matter less, but because value now lives between transactions… in the part of the lifecycle most lenders still treat as an operational afterthought.

1. Originations are converging. Servicing is fragmenting.

Everyone can buy volume, price to a model & stand up an underwriting engine.

But Servicing?

That’s where the gaps show up:

- Repos

- Remarketing

- Impounds

- Titles

- Total Loss

- GAP

- Vendor ecosystems

Operational drag in these functions now drives more loss volatility than the credit file ever did.

2. Refinance cycles are accelerating

Consumers are:

- Refinancing more often

- Easily switching lenders

- Responding to payment pressure faster

- Using digital channels to shop mid cycle

Origination is no longer a single event.

It’s a loop & Servicing controls it.

3. Used is becoming the profit center

In Auto & Powersports:

- Used margins > new margins

- Used inventory turns faster

- Used financing is more resilient

- Used customers drive higher lifecycle value

The industry is quietly shifting from new –> used as the economic anchor.

And Used performance is driven overwhelmingly by Servicing & Asset behavior, NOT front end pricing.

4. Captives are losing lifecycle share

Banks & CU’s are winning because they:

- Own Servicing

- Own CRM

- Own Refi Triggers

- Own Customer Data

- Own the relationship between transactions

Captives own the front end.

Banks/CUs own the middle. The middle is more valuable.

5. CRM + Servicing loops outperform front end margin

The Lenders who win:

- Own Servicing

- Own Communication

- Own Refi’s

- Own Retention

- Own the next transaction

Origination is episodic. Servicing is continuous. Continuous wins.

6. Asset behavior is now the primary risk driver

Part 2 showed Residual Risk is outpacing credit risk.

Part 3 is the consequence:

IF you can’t manage the Asset, you CAN’T manage the Loss!

Recovery velocity is becoming the new competitive moat.

7. The earliest signals show up in discretionary markets first

Before Auto shows stress, Powersports shows it. Before Prime portfolios wobble, Discretionary portfolios wobble. Before Floorplan cracks in Auto, Floorplan cracks in Powersports.

This bridges into Part 4… The Early Warning System

THE STRUCTURAL IMPLICATION

Servicing isn’t just operational anymore. It’s the primary risk engine, the primary customer ownership engine, & increasingly the primary profit engine.

Servicing platforms may become more strategically valuable than lending platforms.

The lenders who build lifecycle ownership, not just origination, will own the next decade.

Part 4 next!

Servicing Solutions – VP, Loss Mitigation | Auto, Lease & Powersport Finance | Risk & Recovery Strategy | LGD, Remarketing & Portfolio Performance

–

–

–

Related:

Ahead of the Curve — Part 2 – Residual Risk Is the New Credit Risk

Ahead of the Curve: Part 1 – Payment Elasticity is the Real Constraint

Servicing Is Eating Originations – Ahead of the Curve Part 3 – Servicing Is Eating Originations – Ahead of the Curve Part 3 – Servicing Is Eating Originations – Ahead of the Curve Part 3

Servicing Is Eating Originations – Ahead of the Curve Part 3 – Delinquency – Bankruptcy – Lending – Auto Loan – Credit Union Collections – Credit Union Collectors – Repossession – Repossess – Repossession – Remarketing

More Stories

Credit Unions Can Now Share More Fraud Intelligence Than Ever Before

Feds Charge 83-Year-Old Woman in Alleged $10 Million Auto Lending Ponzi Scheme

The Great Delay Reaches the Courthouse

Auto Loan Fraud Losses Have Tripled, But the Number of Fraud Cases Is Falling

A Different Kind of Money Laundry

Federal Banking Agencies Issue New Guidance on Immigration-Related Credit Risk