The Bureau’s overhaul of its complaint portal may be less about improving efficiency, and more about fixing a system that became a weapon for credit manipulation.

Did the CFPB Accidentally Create the Credit Washing Industry?

For years, the Consumer Financial Protection Bureau (CFPB) promoted its Consumer Complaint Portal as a powerful tool for consumers who believed financial institutions had treated them unfairly. But according to the Bureau itself, the system had evolved into something very different.

Last week, the CFPB announced a sweeping overhaul of the complaint process, citing “integrity,” “standardization,” and statutory compliance after complaint volumes exploded, particularly in credit reporting. The Bureau says the changes are intended to ensure complaints come from legitimate consumers with legitimate disputes, rather than from automated or abusive submissions.

While much of the initial coverage has focused on regulatory procedure, there is another question worth asking:

Did the CFPB’s own complaint system unintentionally fuel the growth of the credit washing industry?

From Consumer Protection to Business Model

Over the past several years, “credit washing” evolved from a niche tactic into a multimillion-dollar business.

The concept is simple.

Companies advertise that they can quickly improve a consumer’s credit score by disputing virtually every negative tradeline appearing on a credit report.

Many charge hundreds, or even thousands, of dollars for the service.

Rather than carefully evaluating whether information is inaccurate, some firms simply submit mass disputes hoping creditors will fail to verify the account within required timeframes.

If the furnisher does not respond quickly enough, the item may temporarily disappear.

The CFPB’s complaint portal became an attractive second step.

When routine disputes failed, some companies encouraged consumers to file CFPB complaints, knowing many financial institutions treat Bureau complaints with far greater urgency than ordinary credit disputes.

In effect, the federal complaint process became another escalation tool in a commercial credit repair strategy.

An Explosion the CFPB Could No Longer Ignore

The numbers tell the story.

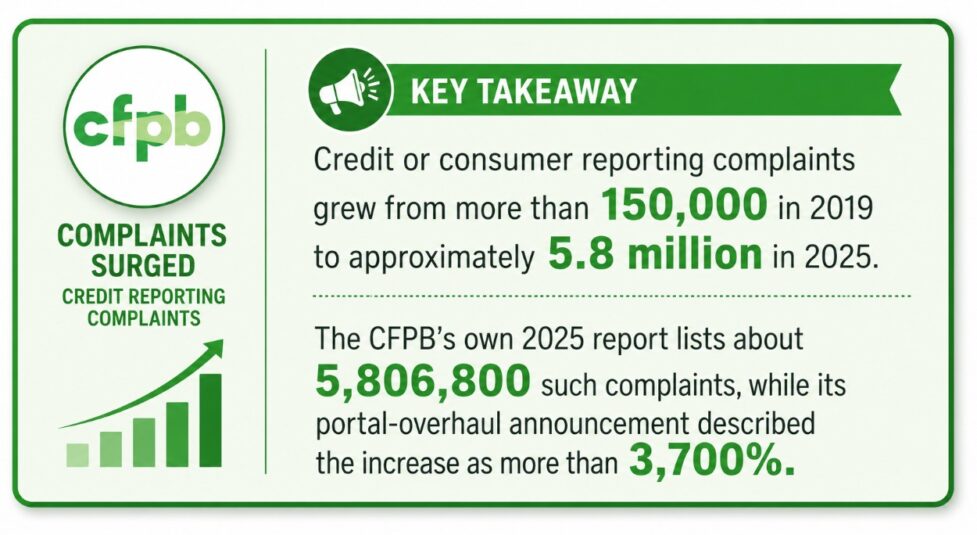

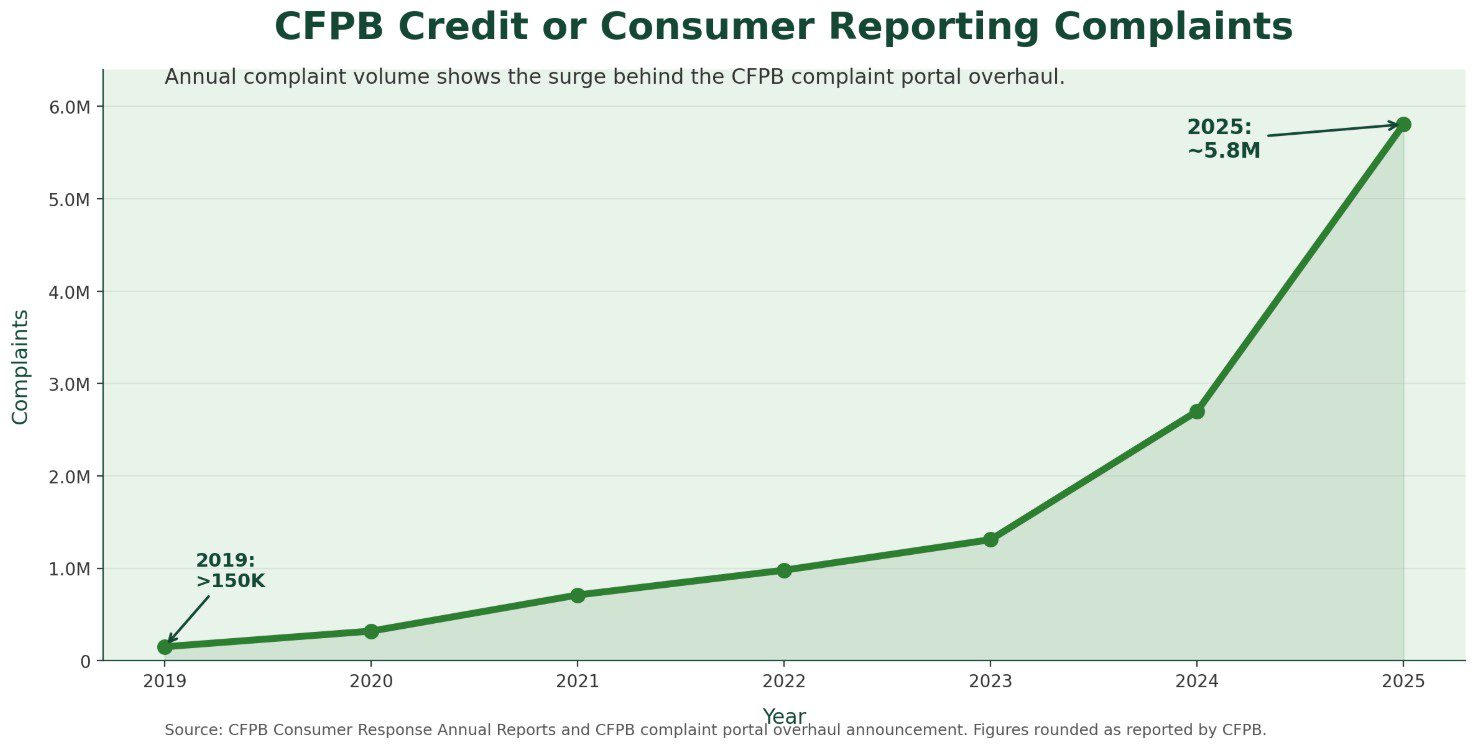

According to the CFPB, annual credit reporting complaints increased from roughly 150,000 in 2019 to more than five million in 2025, an increase so dramatic the Bureau concluded the system’s usefulness had been compromised.

The agency now says complaint quality deteriorated as mass-produced submissions overwhelmed legitimate consumer concerns.

Among the reforms announced:

- stronger identity verification through two-factor authentication;

- greater emphasis on consumers first exhausting normal dispute channels;

- standardized complaint intake;

- additional screening to identify abusive or duplicate submissions; and

- directing agency resources toward complaints warranting substantive review.

Those changes sound administrative.

In reality, they may represent one of the Bureau’s strongest acknowledgments yet that the complaint system had become vulnerable to organized abuse.

Credit Washing’s Impact Extends Beyond Lenders

Credit washing is often portrayed as a problem only for banks and credit bureaus.

It isn’t.

For auto lenders, manipulated credit reports can lead to loans being approved that otherwise would have been declined or priced differently.

Higher-risk borrowers may appear less risky than they actually are. When those loans default, the effects ripple across the entire recovery ecosystem.

Credit unions, finance companies, repossession agencies, remarketers, and ultimately consumers all absorb higher losses.

Artificially improving a borrower’s credit profile doesn’t eliminate underlying financial distress. It merely delays recognition of the risk.

Did the CFPB Incentivize the Behavior?

The difficult question isn’t whether credit washing exists. It clearly does. The harder question is whether federal policy unintentionally encouraged it.

The CFPB never intended its complaint system to become part of commercial credit repair operations.

Yet the Bureau publicly displayed complaint statistics, highlighted company response rates, and created an escalation path that many consumers, and some credit repair businesses, viewed as more effective than the traditional dispute process.

Over time, filing a CFPB complaint became almost routine advice across online forums, social media, and credit repair marketing.

Once that happened, the complaint portal arguably shifted from being a consumer protection mechanism to becoming leverage in private credit disputes.

That doesn’t mean the Bureau caused credit washing. But it may have created incentives that made the practice easier to scale.

A Necessary Course Correction

Consumer advocates worry the new rules could make it harder for legitimate consumers to obtain help. That concern deserves serious consideration.

Not every spike in complaints represents abuse, and consumers still need an accessible avenue when credit reporting errors genuinely exist. However, the Bureau appears to have concluded that the system reached a tipping point where quantity overwhelmed quality.

If millions of complaints are generated by automated processes, duplicate filings, or commercial credit repair campaigns, the complaints most deserving of attention inevitably compete for limited resources.

Ironically, that may leave the very consumers the CFPB was created to protect waiting longer for meaningful assistance.

Why Credit Unions Should Pay Attention

For credit unions and auto lenders, this policy shift extends well beyond regulatory housekeeping. It signals federal recognition that complaint systems, like credit reporting itself, can be manipulated when incentives become misaligned.

Lenders should expect greater scrutiny of dispute documentation, closer examination of repetitive complaint patterns, and renewed emphasis on direct consumer engagement before regulatory escalation.

For institutions battling first-party fraud and credit washing, those changes may help restore confidence that legitimate disputes receive attention while organized manipulation becomes more difficult.

Whether the reforms succeed remains to be seen.

But one conclusion is increasingly difficult to avoid:

The CFPB isn’t simply redesigning a complaint portal. It appears to be repairing a system that, despite good intentions, may have become one of the most effective tools the credit washing industry ever had.

The CFPB isn’t simply redesigning a complaint portal. It appears to be repairing a system that, despite good intentions, may have become one of the most effective tools the credit washing industry ever had.

Did the CFPB Accidentally Create the Credit Washing Industry? – Did the CFPB Accidentally Create the Credit Washing Industry? – Did the CFPB Accidentally Create the Credit Washing Industry?

Did the CFPB Accidentally Create the Credit Washing Industry? – Credit Union Collections – Credit Union Collectors – Fraud – Fraud – Consumer Financial Protection Bureau – CFPB

More Stories

The Auto Finance Paradox

Early Bird Registration for CCUCC 2026 Ends August 14

Point Predictive Releases Q2 2026 Fraud Risk Intelligence Report

18 Year Old Fraud Auto Loan “Credit Mule” Busted on Video

Closing the 30-Day Blind Spot: How Lenders Can Shut Down Auto Loan Bust-Out Fraud

Editorial: TCPA – The Law Technology Left Behind