Wisconsin Case Raises New Questions About Dealer Verification, Wire Transfers, and Credit Union Liability

When a Loan Funds a Scam: Who Bears the Loss?

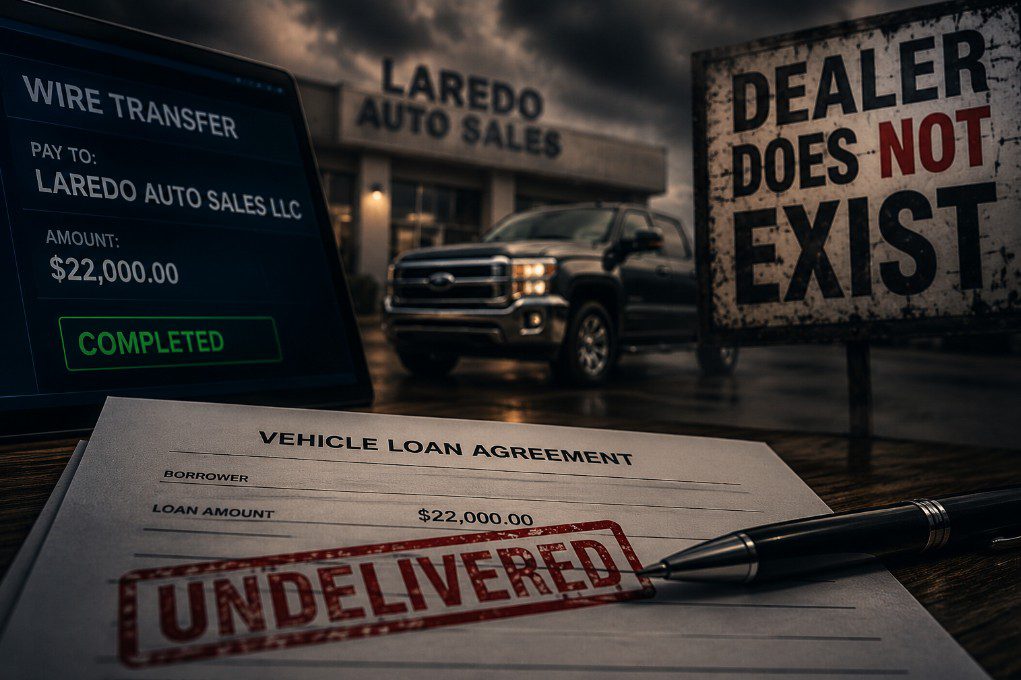

Hartford, WI – June 26, 2026 – A Wisconsin man’s claim that his credit union wired more than $22,000 to a fraudulent vehicle dealership before holding him responsible for the loan is drawing attention to a growing risk facing financial institutions as more vehicle purchases move online. While law enforcement is treating the incident as a criminal fraud, the circumstances also raise broader questions about lender due diligence, wire transfer controls, and the allocation of financial responsibility when a financed purchase never materializes.

According to a report by Milwaukee television station TMJ4, Hartford, Wisconsin resident Billy Heck says he located a 2019 Chevrolet Silverado advertised by what appeared to be a legitimate dealership in Laredo, Texas. After obtaining financing through Landmark Credit Union, loan proceeds were wired to the dealership. The truck never arrived, the dealership’s website disappeared, and Heck later learned he had allegedly been the victim of an elaborate scam.

Heck told TMJ4 that the dealership appeared authentic, complete with an online inventory, business registration, reviews, and what appeared to be a legitimate banking relationship. According to emails he provided, a loan specialist at Landmark Credit Union reportedly verified aspects of the dealership before recommending that funds be sent via wire transfer because the dealer required payment before shipping the vehicle.

After the vehicle failed to arrive, Heck says he notified the credit union that he believed both parties had been scammed. He alleges the institution ultimately informed him that while he was not considered at fault for the fraud itself, he remained legally responsible for repaying the approximately $22,000 loan. He says the credit union later agreed to remove the loan’s interest but not the principal balance.

Landmark Credit Union declined to discuss the specific customer matter publicly, citing privacy obligations. However, following inquiries from reporters at TMJ4, the credit union issued statements confirming that it had initiated a formal internal review and that it maintains “zero tolerance for misconduct.”

Beyond Consumer Fraud

Although the facts surrounding the fraud itself are unusual, legal professionals say the more significant questions may involve how the loan proceeds were disbursed and what responsibilities each party held during the transaction.

Consumer vehicle loans typically place responsibility on borrowers to identify the vehicle they wish to purchase and to enter into the purchase agreement. However, once a lender disburses funds directly to a dealership, particularly through a wire transfer, the institution’s own verification procedures may become part of any subsequent legal analysis.

Among the questions attorneys would likely examine are:

- What dealer verification procedures were performed before funding?

- Were the dealership’s banking instructions independently authenticated?

- Did the lender follow its own internal wire transfer policies?

- Were additional safeguards required because the transaction involved an out-of-state dealer?

- Were there warning signs that reasonably should have prompted additional review?

The answers to those questions could become important if the borrower pursues civil claims or if regulators review the institution’s lending practices.

Comparative Responsibility

The case also highlights an issue that has become increasingly common as fraud schemes become more sophisticated: multiple victims can exist within the same transaction.

The borrower lost the opportunity to purchase a vehicle and remains obligated on a loan. The credit union appears to have lost the loan proceeds paid to an alleged fraudster. Meanwhile, the criminals responsible may never be identified.

If litigation were filed, a court could be asked to determine whether responsibility rests entirely with the borrower, entirely with the lender, or whether liability should be shared based on each party’s actions. Wisconsin’s comparative negligence framework allows fault to be apportioned among multiple parties depending on the specific facts presented.

A Growing Risk for Online Vehicle Purchases

As more vehicle purchases originate through online marketplaces and remote dealerships, financial institutions increasingly rely on electronic communications, digital documentation, and wire transfers to complete transactions.

Those conveniences have also created new opportunities for sophisticated impersonation schemes that mimic legitimate dealerships with convincing websites, business registrations, and even authentic-looking banking relationships.

For lenders, the case serves as a reminder that dealer verification procedures and wire transfer controls may become just as important as traditional underwriting standards in preventing fraud losses.

Lessons for Credit Unions

Whether Landmark Credit Union ultimately bears any legal responsibility remains unknown, and no court has made findings regarding liability. However, the circumstances illustrate several practical questions every credit union should consider:

- Are dealer verification procedures sufficient for remote transactions?

- Should additional authentication be required before wiring loan proceeds?

- Are lending staff adequately trained to recognize increasingly sophisticated dealership impersonation schemes?

- Do existing policies clearly define when wire transfers should, or should not, be used to fund vehicle purchases?

As vehicle sales continue shifting toward digital transactions, cases like this suggest that fraud prevention may increasingly depend not only on evaluating borrowers, but also on verifying who receives the money.

For credit unions, the incident is less a story about one unfortunate loan than a reminder that in today’s lending environment, operational controls surrounding disbursement may be every bit as important as credit underwriting itself.

I particularly like this story because it highlights an emerging risk that hasn’t received much attention in the credit union space. We’ve written extensively about identity theft, synthetic fraud, and first-party fraud, but dealer impersonation fraud is different. It attacks the funding process itself rather than the borrower. As more lenders finance vehicles purchased entirely online and across state lines, I suspect we’ll see more cases like this unless dealer verification and wire-transfer authentication become much more robust.

Source: (TMJ4 News)

When a Loan Funds a Scam: Who Bears the Loss? – When a Loan Funds a Scam: Who Bears the Loss? – When a Loan Funds a Scam: Who Bears the Loss?

When a Loan Funds a Scam: Who Bears the Loss? – Credit Union Collections – Credit Union Collectors – Lending – Fraud – Auto Loan – Lending

More Stories

Early Bird Registration for CCUCC 2026 Ends August 14

Point Predictive Releases Q2 2026 Fraud Risk Intelligence Report

18 Year Old Fraud Auto Loan “Credit Mule” Busted on Video

Credit Union Collection Professionals Announces 2027 CUCP Summit in San Antonio, Texas

Closing the 30-Day Blind Spot: How Lenders Can Shut Down Auto Loan Bust-Out Fraud

Editorial: TCPA – The Law Technology Left Behind